In Search of Market Tremors...

Concerns arise over treasury market liquidity, why volatility could be a virtue to central banks, another intervention occurs, and Goldman rethinks shelter inflation...

Welcome back to Market Making, your weekly dose of sell-side research and insight.

⏱️ Estimated Read Time: ~37min

✍️ Word Count: ~8,010

📚 This week’s Reading List has been updated

Part 1: Nerves Fray as the Treasury Market Sways

In the wake of the BoE’s successful intervention into the long-dated gilt market, market participants have begun to look around for hairline cracks that could expand out further under continued rate-hike stress.

So, in recent weeks a narrative has begun to arise that the treasury market - the world’s deepest market, not to mention most important - is showing signs of worrying levels of illiquidity and that some level of action is needed.

As I’ve argued in past weeks - when dismissing concerns around equity market liquidity - it’s axiomatically true that when asset prices decline and volatility rises that liquidity diminishes. This, at face value, shouldn’t cause concern and the reactionary rhetoric in the face of more illiquid conditions is largely a function of having livid through such a long period of volatility suppression after the financial crisis.

However, it’s likewise axiomatically true that any significant market reaching levels of dangerous illiquidity has the capacity to precipitate an entirely unnecessary financial crisis and, when such scenarios arise, intervention is entirely warranted.

This is why I was entirely supportive of the BoE’s actions several weeks ago and was quick to distinguish what occurred from more traditional forms of quantitative easing.

However, here’s the rub when it comes to treasury market illiquidity: the Fed would never allow the treasury market to reach levels even approaching true illiquidity due to the severe levels of financial instability that would be unleashed as a result.

By extension, this means that if the Fed came to the conclusion that the treasury market was at risk of becoming truly illiquid, it would need to take swift and decisive actions to avoid that (i.e., the Fed would need to act proactively, not reactively).

Glazing over lots of nuance, the quickest way to inject liquidity into the system would be for the Fed to:

Signal that they’re no longer raising rates as that would immediately create more bids for treasuries (as you would know that after you buy treasuries their yields would be less likely to spike significantly higher, thus causing you less concern regarding taking significant mark-to-market loses).

Signal that they’re stopping quantitative tightening or may even begin more specific forms of targeted quantitative easing (i.e., similar to the BoE’s successful operations over the past few weeks).

It’s becoming increasingly clear that many market participants understand this reaction function and that if you want the Fed to blink, even in the face of continuing inflationary pressure, one way to do that is to make the Fed believe that they’re introducing untenable levels of financial instability through their policies.

…And the single biggest form of financial instability the Fed could induce through its current policies is a breakdown in the treasury market.

This is not to say that there aren’t serious people who are seriously concerned about the treasury market — that’s certainly the case, including myself! However, there are many more people who are naturally long the market - whether in rates, credit, or equities - who want to see the Fed pivot and these people seem suddenly and suspiciously concerned about treasury market volatility.

Breakdowns and Blackouts…

Throughout the past week yields across the curve were rising, largely in tandem, with slightly higher bid-ask spreads than normal — but nothing that caused any degree of meaningful chatter.

The sell-off across the curve was entirely orderly and largely moved for the same reasons that the curve has moved for the past year: higher than expected inflation, a stronger than expected labor market, and stronger than expected growth.

However, by the end of the week the curve ended up steeper by around 35bps, the most steepening in a week since January of 2009…

The dramatic moves in yields we saw on Friday - which included 2s30s steepening 20bps alone, driven almost exclusively by a rally in the two-year - was precipitated by two things.

First, Nick Timiraos of the WSJ wrote a piece detailing how the Fed was planning on moving by 75bps in November but saw the meeting as an opportunity to layout a framework for reducing the pace of rate hikes with 50bps being more likely in December.

Given Timiraos’s reputation as a Fed whisperer (i.e., someone who members of the FOMC strategically leak to in order to prepare the market for future actions) this caused a swift and immediate reaction in front-end yields and risk assets.

Most notably the December meeting rate hike expectations, which were pricing in a 70% chance of 75bps, immediately fell to 30%. Which puts the number roughly in line with where it was prior to the hotter-than-expected CPI print last week — that’s partly why I argued for “looking through” that CPI print, a lot can happen before December!

Given how transparently the Fed has leaked to Timiraos in the past, it’s quite clear that the Fed was hoping to prepare the market for a slower pace of hikes without causing an immediate loosening of financial conditions (as happened over the summer) by confirming that they would be doing 75bps in November.

But given that equities ended up with their best week since June - after the NDX was nearly -1% pre-market on Friday - the market seemed not to catch onto that nuance.

Second, the Fed’s Daly gave a speech in which she mirrored the sentiment of Timiraos’s reporting — suggesting that the Fed needed to be cautious about overdoing rate hikes and that a step-down in rate hikes will be needed eventually.

Further, Daly proactively brought up that any possible future intervention by the Fed into markets is not necessarily equivalent to quantitive easing. While I’m in full agreement with this sentiment, proactively saying this with so little qualification has the obvious impact of spurring risk assets as it’s functionally saying there will be a “Fed put” if some markets grow disorderly (i.e., the treasury market).

What makes all of this more notable is that the Fed’s blackout period - in which no Fed member will be giving speeches or be making comments - began on October 22 and will run through November 3 (the Thursday following the FOMC meeting).

So the mix of Fed rhetoric we got Friday - which was decidedly dovish - can be thought of as trying to set the tone into the meeting. However, if we get a strong market rally in risk assets into the FOMC meeting, the Fed may decide to pull another Jackson Hole and talk down the market once again.

Further, it’s worth considering whether or not the rhetoric we got on Friday was due to just how much yields across the curve were rising through the week. In the wake of what happened in the UK, the Fed could have been worried that yields would grind even higher running up to the meeting — perhaps to the point of causing some modest dislocations during the blackout period.

The Forces of Illiquidity…

Several weeks ago I mentioned that whenever Jeff Currie of Goldman speaks, he’s worth listening to even if you aren’t that interested in oil and gas. Likewise, whenever Mark Cabana of Bank of America speaks about treasuries, he’s worth listening to.

This week Cabana came out with a note titled, “Liquidity is a Privilege, Not a Right”. The central argument that Cabana makes throughout is that while the treasury market has been fortunate to have limited illiquidity issues in the past, there’s no guarantee that’ll persist into the future.

And with huge amounts of supply coming online, many natural treasury buyers retreating, macroeconomic uncertainty, and rate hikes expectations still marching higher there’s becoming ominous signs of stress within the treasury market.

So let’s set the stage…

Cabana opens his note by referencing Secretary Janet Yellen’s comments last week that there has been a “loss of adequate liquidity” in the treasury market and saying that he agrees with that.

However, it’s clear that Cabana isn’t as concerned with where we are now (i.e., he doesn’t really think there’s an inadequate level of liquidity currently). Rather, he’s concerned that the treasury market is relatively fragile and that a sizeable shock could lead to substantial illiquidity and financial dislocations (i.e., a crisis).

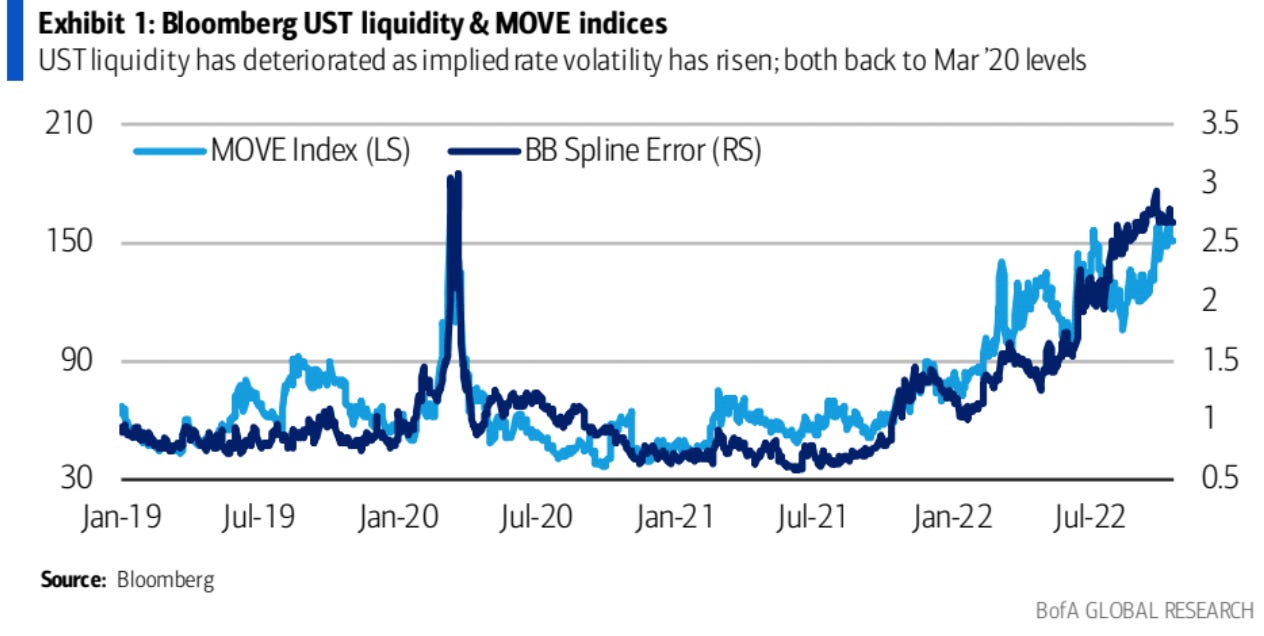

Anyway, there are a number of ways you can think about measuring illiquidity. In the popular press you’ll frequently see people discussing the level of implied volatility in treasuries - as measured by the MOVE index - which is at highs not seen since the pandemic.

Indeed, Cabana starts off his note with this index — although it should be noted that during the financial crisis MOVE reached around 250, so we’re still a long way from that. Further, you’d expect vol during a fast rate hike cycle as, obviously, increasing rates will move prices thus creating volatility — volatility isn’t inherently a bad thing!

Personally, I’d be somewhat reluctant to pay that much attention to volatility induced measures of liquidity. While they tend to be directional correct in signalling illiquidity, they don’t give you a good relative sense of how liquid (or not) conditions are.

In an inflationary environment if you’re trying to measure illiquidity, the most intuitive way to do so would be to look at bid-ask spreads relative to years past. Further, if you see not only that spreads have widened, but that they’ve widened most for long duration or off-the-run treasuries, then you know markets are truly getting substantially more illiquid.

The Fundamental Factors Driving Illiquidity…

As with nearly any period of illiquidity that hits a market, there’s a combination of fundamental and technical factors at play. So let’s start with what matters most, the fundamental factors…

There’s no doubt that the treasury market is facing a continued onslaught of supply (originating from the deficits still being extremely large by any measure) along with no natural marginal buyer stepping in.

This latter point has been driven by a number of factors, but let’s quickly highlight two of them:

First, foreign buyers (i.e., pension and life insurance funds) used to be significant marginal buyers given how low their domestic yields were relative to the US. However, with a global tightening cycle occurring nearly everywhere, there’s been naturally less interest from these players as they can just park their money at home more and not worry about hedging out their currency exposure through swaps.

Second, as we covered when discussing UK pension funds, the way many earn a sufficient return to meet their future obligations is via levering up a pool of long-duration governments bonds (to get the right asset / liability matching) and then putting the rest of their assets into riskier investments (primarily equities).

Part of how the overall vol is compressed in this kind of portfolio makeup is through the historically negative relationship between bonds and equities (whereby when equities rise in a growing economy that tends to send yields higher too).

However, the market over the past year has begun to be governed by a different set of norms that are driven exclusively by Fed policy. Now all assets tend to trade in the same direction - in price terms - based on whether the prevailing sentiment is risk-on or risk-off.

So, for example, as equities have fallen due to the Fed trying to tame inflation, that has naturally led to yields across the curve rising, which has sent treasury prices down.

The natural consequence of this is that now any large asset manager - whether domestic or foreign - that wants to limit vol in their portfolio will be looking to equity-based hedges as opposed to the more traditional hedges via buying fixed income instruments (i.e., treasuries).

Part of why I’ve found the discussion around treasury market illiquidity frustrating is that many have entirely disregarded these fundamental factors — as if what is driving illiquidity is something technical and easily fixable, as opposed to being driven by rational actors making rational decisions (i.e., asset managers saying to themselves, “let’s not buy treasuries because they aren’t acting as a hedge and yields are likely to keep going up thus making up lose even more money!”).

The Technical Factors Driving Illiquidity…

One way to frame the distinction between the fundamental factors and the technical factors driving illiquidity is that it’s not really possible to change the fundamental factors unless there’s a wholesale change in monetary policy.

Which is part of the reason much of the treasury market illiquidity conversation is frustratingly artificial — all the liquidity being “missed” will return like water breaking from a dam when the Fed does begin to lower rates, and a non-trivial amount will probably come back as the Fed reaches their terminal rate and pauses.

However, Cabana does list some technical factors that could alleviate some of the heightened levels of illiquidity we’re observing now — although some of these are so minor as to hardly make a difference.

We won’t go through all of these, as most are self-explanatory (Central Clearing of USTs), not likely to make a difference (Treasury Transparency), or not likely to ever happen (Dealer of Last Resort).

However, there are a few that I’d point out…

SLR for USTs…

The SLR is the implementation of Basel III’s Tier 1 leverage ratio (dictating the amount of equity that must be held by a bank relative to their “total leverage exposure”).

However, the SLR is not weighted by risk by design as it’s meant to be a kind of minimum requirement that banks must uphold regardless of how few risky assets they’re holding on their balance sheet.

The rationale behind this is that often risks can manifest themselves from supposedly risk-free assets (i.e., long-duration gilts!) so it shouldn’t be the case that by virtue of holding predominately or exclusively risk-free assets that banks can have very high degrees of leverage.

The Supplementary Leverage Ratio (SLR) was modified in the wake of the pandemic to exclude treasuries, which proved to help stabilize the treasury market significantly at the time.

The real source of technical illiquidity - in my view - is emanating from large dealers (i.e., Cabana’s own Bank of America) reducing down their treasury holdings significantly and especially not wanting to hold off-the-run securities.

Making modifications to the SLR - whether that means an outright exclusion of treasuries from its calculation, or weighing treasuries much less - is a clear and obvious way to allow dealers to hold more treasuries and better make markets for clients.

…But you try telling regulators to allow for supposedly “enhanced leverage” to be undertaken by systemically important financial institutions. The Fed was reluctant to endorse the idea even in the midst of the pandemic and treasury vol exploding.

Treasury Buybacks…

The Treasury Borrowing Advisory Committee (TBAC) is made up of various sell-side and buy-side market participants. They meet with the Treasury every quarter to give their inside perspective on market functioning and how best the Treasury can manage the issuance of future debt efficiently and effectively.

The Treasury Department undertaking buybacks had been discussed at TBAC meetings recently in February 2015 and August 2022, although the Treasury ultimately opted not to pursue them.

There are a myriad of ways that buybacks could occur but the general aim would be to do two things: improve market functioning and lower the overall cost of debt.

So what the Treasury would do is buy back cheap off-the-run securities - which is where illiquidity always manifests first, thus why they’re slightly cheaper - and fund that through the issuance of new securities (which will be, by definition, on-the-run).

However, the question then arises as to where the Treasury decides to issue new securities to fund the buybacks. While they could try to issue new securities such that the duration of those issued matches those bought, they could also issue short-term debt (i.e., t-bills) that have significantly lower yields than long-duration off-the-run securities.

This would boost liquidity in the front-end of the curve, capture the trading discount of long-duration off-the-run securities, and provide a lower on-going debt servicing cost relative to issuing new long-duration debt (given the relative steepness of the yield curve).

An under-rated aspect of this latter point is that you would have the Treasury making significant buys out the long-end, but not doing significant selling of new-issuance of the same duration to match. This would have the effect of likely lowering yields out the long-end (prices up, yields down on higher demand).

Given what we’ve already discussed regarding the risk-on / risk-off way in which markets are currently trading, any operation that lowers yields - whether through the Treasury doing buybacks, or the Fed doing any form of buying - would likely lift risk assets significantly.

Note: The last time the Treasury did buybacks was back in 2000-2002. But their rationale for doing so was because the government was running surpluses, so there was limited new issuance of debt. So in order to maintain orderly markets when there was a lack of supply (not lack of demand, like today!) they decided to buy off-the-run securities which they funded through new on-the-run securities of a similar duration.

Where there’s smoke, there’s often fire — and over the past week there’s been increasing chatter about the Treasury finally moving forward with buybacks two decades after last doing so under very different conditions. This has resulted in old 20-year treasuries outperforming over the past week as everyone jostles to figure out where the Treasury would first be looking to do the buybacks.

Goldman anticipates that for the buybacks to be meaningful and worthwhile, the operation would need to be around $200-250b in size. However, Goldman is more skeptical on whether this will improve liquidity (i.e., bid-ask spreads) as it just places a temporary bid under illiquid issues (the majority of which won’t be bought by the treasury, given the huge amount outstanding) and introduces a large amount of new supply that needs to be absorbed by someone (although there would likely be much more demand for the kinds of supply being introduced if it’s short-duration).

Nervous, Neurotic, or Neither?

The reality is that messaging around future events that could heavily impact the treasury market - whether on the fiscal policy side or, most often, the monetary policy side - are often first disseminated through the media to avoid shocking markets too heavily when they are officially announced.

This is a cause of perennial consternation and was on full display when Nick Timiraos published his "reporting” on Friday which caused a reaction - between the moves in rates and equities - in the hundreds of billions. It’s understandable to think that a reporter being able to sway markets like that is somehow untoward.

However, the use of “leaking” to the media does serve a useful function of sending out a trial balloon on potential future actions to see how markets react or if valid criticism is raised.

For example, if risk-assets catch a strong bid during the Fed’s blackout period - causing financial conditions to loosen - that will play a role in the messaging of the Fed after the meeting as they try to get markets prepared for lessening, but still continuing, rate hikes moving forward.

The counterfactual that needs to be considered is that yields were spiking across the curve prior to Friday quite significantly. If that continued through the blackout period, markets could have ended up verging on being disorderly.

In my mind, reading the tea leaves as best I can, it’s hard not to look at the messaging over the past few weeks and to think that some within the Fed and Treasury are getting a bit spooked, and that they’re uncomfortable with how quickly yields have moved upwards in the wake of the BoE’s intervention and the instability being shown in other markets like Japan (where multiple currency interventions have occurred).

So when I see Yellen make a statement that there has been a “loss of adequate liquidity” in the treasury market, I don’t take it at face value. There’s no one who really believes there’s inadequate liquidity — the market is functioning! Rather, it signals that there is a concern about the risk for a loss of adequate liquidity to develop and for financial instability to arise as a result.

Curiously, we’ve now had pieces in the popular press along these lines…

Barron’s, The Treasury Market Could Seize Up. That Could Be Disastrous for Everyone. By Lisa Beilfuss, formerly of the WSJ.

Bloomberg, The Fed’s Next Crisis Is Brewing in US Treasuries. By Robert Burgess, the executive editor of Bloomberg Opinion, formerly executive editor of financial markets.

Paired with the speech by the Fed’s Daly - suggesting that intervention in markets is not tantamount to reengaging in quantitive easing - there’s clearly a bit of telegraphing occurring here.

So here’s the thought experiment that everyone needs to be considering…

It’s unequivocally true that it’s untenable to allow true dislocations to develop in the treasury market, so preemptive action will need to be taken. You can’t be reactive to the most liquid market in the world becoming truly illiquid.

But the issue with taking preemptive action is always that you don’t know for sure if the thing that you thought was going to happen (the market becoming illiquid) would’ve happened without you taking action.

However, what is axiomatically true is that taking strong action in the treasury market - whether on the fiscal or monetary side - will reduce any risk premium embedded in yields right now and have the effect of loosening financial conditions, which would then add some additional fuel to the ongoing inflationary fire.

As we’ve discussed previously, my strong conviction is that while some technical solutions can enhance liquidity, the only way to restore the market to some level of normality is through a much slower pace of hikes or an out-right pause. That’s what will draw back in marginal players in size.

My equally strong conviction is that some market participants who are beating the treasury market illiquidity drum are doing so because they view this as the best way to get the Fed to blink — because while they may not blink in the face of declining equity markets or increasing unemployment, they will at treasury market instability.

Part 2: Is Volatility a Virtue?

Last week I rather forcefully defended Governor Bailey’s decision to foreclose any possibility of extending the BoE’s market intervention, along with the strong rhetoric he used in doing so.