No Premature Pausing...

Powell breaks out his hawkish handbook, a legendary hedge fund doesn't like what it sees, and the BoE begs the market to reconsider the yield curve...

Welcome back to Market Making, your weekly dose of sell-side research and insight.

⏱️ Estimated Read Time: ~41min

✍️ Word Count: ~8,860

📚 This week’s Reading List has been updated

Part 1: Powell Proves Prescient

In the first part of last week’s newsletter I didn’t mince words about the kind of self-manufactured quandary that the Fed had put itself in. By trying to talk down yields on October 21 - just prior to the onset of the Fed’s blackout period - they inadvertently sparked a loosening of financial conditions during the next week so extreme that it had only been seen a few times before this century.

There were many ironies to this episode — not least being that this meeting was likely the ideal time to communicate that the Fed would be stepping-down the pace of its rate hikes. After all, even the most hawkish market participants would concede that rate hikes of 75bps can’t continue ad infinitum and that rates are now solidly approaching restrictive levels.

But the Fed’s actions prior to the blackout contributed significantly to the narrative surrounding a globally coordinated campaign to soon start pausing rate hikes being underway. This then made it difficult to envision the Fed being able to credibly signal stepping-down the pace of hikes at this meeting without further accelerating the loosening of financial conditions that was already occurring.

Here’s a snippet of what I wrote last week…

Given that we’ve only had a week of significant loosening in financial conditions the question is now whether Powell can see that the market is poised for, as Goldman said, the most violent (upwards, risk-on) set-up we’ve had all year.

The market is ready to materially lower credit spreads, pummel the dollar, beat down treasury yields, and make equities fly — it’s just waiting for permission from Powell to do so.

After the release of the FOMC statement, it appeared that markets had gotten exactly what they sought: the insertion of modestly dovish language that was a clear nod toward likely slowing the pace of hikes moving forward.

As a result, credit spreads did begin to tighten, the dollar did fall, treasury yields did get beat down, and equities did fly. But there was caution in the air as markets waited for Chair Powell, at his press conference just thirty minutes later, to confirm and endorse the modestly dovish language contained in the statement.

But Powell had learned a lesson after he sparked a massive loosening of financial conditions this summer by saying the Fed had reached its neutral rate, only then to backtrack at Jackson Hole almost exactly a month later.

Here’s the lesson: when markets are agitating to loosen financial conditions, and you’re trying to tighten them, then you don’t give an inch, you don’t leave room for ambiguity, and you don’t go off-script. Because if you do, then the impact of your hiking will begin to be unwound by a loosening of financial conditions.

To properly set the events surrounding the rate hike in context, along with the market reaction to it and what stood out to me the most in Powell’s press conference, let’s try to move sequentially through what happened this week…

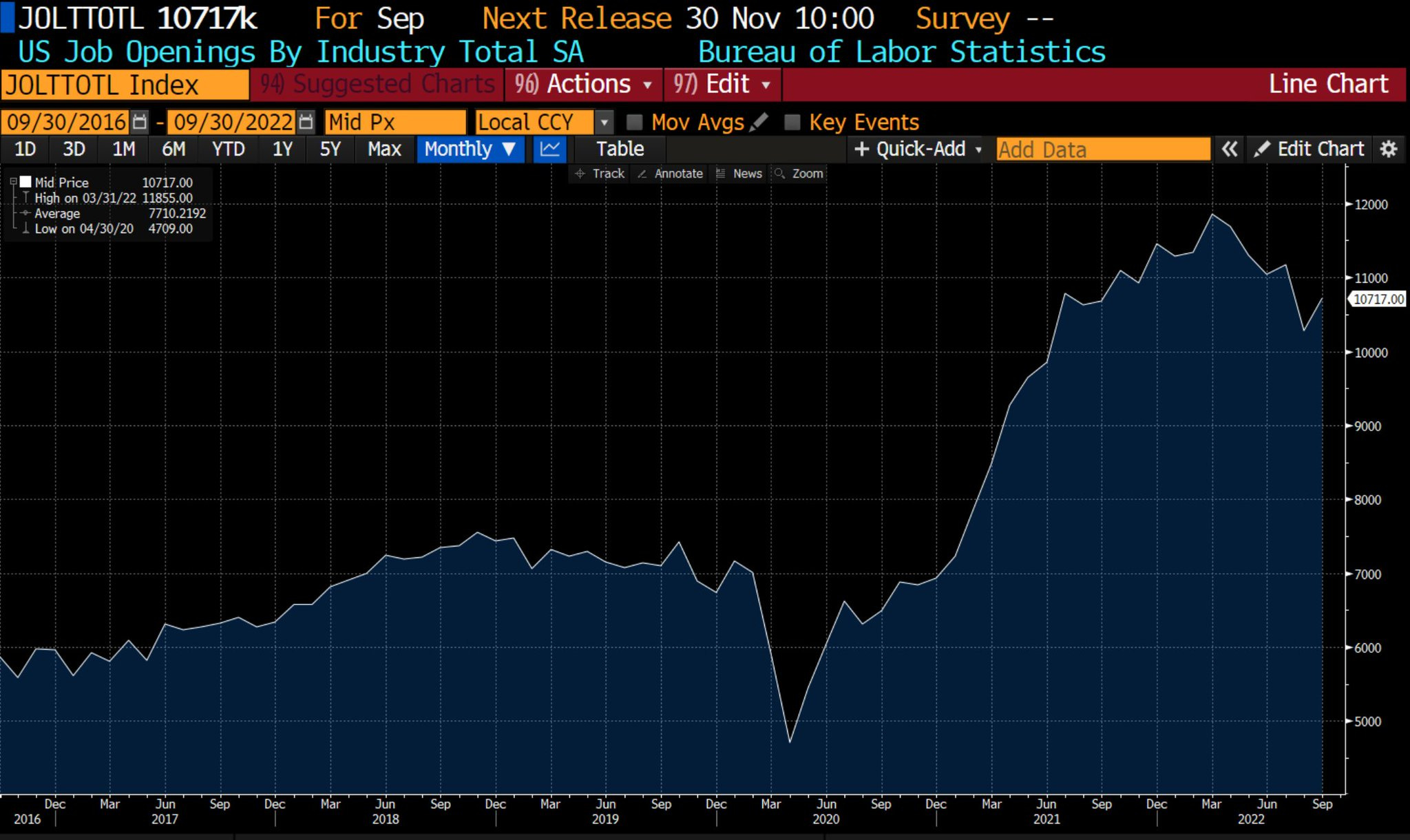

Tuesday: JOLTS Day…

At the end of last week’s newsletter I highlighted some of the economic data being released that I thought was of particular importance, including the JOLTS release.

Part of the reason why there are wildly divergent views on how likely a recession is next year - with Bloomberg saying it’s 100% and Goldman saying it’s around 30% - comes down to how meaningful you find JOLTS data and how much you think can be inferred from its sizeable monthly swings.

The Fed, along with Goldman, have the view that if job openings can come down from their historically elevated levels fast enough then that could lead to the goldilocks scenario in which wage inflation cools without necessitating much higher unemployment.

The rationale is simple and intuitive: if you’re looking for a new job and there are ten comparable postings, then you have some implicit form of bargaining power and will likely go with whoever pays you more. Likewise, if you’re currently employed by a firm and they don’t give you a large enough raise, but there are ten comparable postings, then you may leave your current firm and go take a new higher-paying job.

However, if there’s only one comparable job posting that would be applicable to you, then the wage dynamic shifts: suddenly the comparable job poster only needs to offer you a marginal increase over what you’re earning right now as they’re only competing with your current employer.

Goldman has a model for thinking about just how much the job-workers gap needs to close to be consistent with the Fed’s inflation target, and after the release of the August JOLTS data they said we had seen 50% of the decline necessary.

I would say that most are quite skeptical about just how mechanical the relationship is between the job-workers gap and wage inflation — it’s likely the case that there is some hurdle rate employers have to offer to entice new employees that is more closely associated with underlying inflation.

In other words, to make the disruptive transition over to a new employer worthwhile then you need to be offered a wage increase that materially increases your real wages (i.e., something in excess of inflation). This little mental model not only has more intuitive appeal, but it appears to be borne out in the ADP data that we’ve been getting (the last round was released on Wednesday which we’ll discuss next).

Regardless of your mental model surrounding job openings, one thing is clear: job openings going up from already historically elevated levels represents a clear sign that labor markets are still far too hot to be conducive with the wage inflation declines necessary to get back to target inflation.

So on Tuesday the risk-on sentiment pervading markets began to slightly temper when job openings for September beat everyone’s expectations. Last month’s print for August was 10,053k and the consensus view for this month was 9,750k. Instead, we got 10,717k — the first uptick since May of this year and much larger in magnitude.

Employment is always one of the last shoes to drop in an economic downturn, but we are still a long way away from seeing employment begin to be consistent with the inflation target — even if you’re using Goldman’s model…

Wednesday: ADP Report…

In case there was any thought that the JOLTS release was just a noisy data-series from September - somehow not indicative of what was happening beneath the surface - this was quickly dispelled by the ADP report released on Wednesday covering the private workers added in the month of October.

While goods-producing employment fell, service-producing employment rose sharply. Mirroring the goods-to-inflation rotation that has occurred in inflation…

Many have argued that this print shows an underlying softness to employment given just how uniform the loses were outside of a few areas of service employment. This may well be true - although often employment is lumpy month-to-month - but the market didn’t receive the report well given that the tightest labor market seen in generations was still stubbornly grinding higher.

What caught my eye the most in the ADP report wasn’t the headline number but rather the wage growth that we’re still seeing. More specifically, the high wage growth we’re still seeing in sectors that are rate-sensitive and that have seen an actual drop in employment over the past few months.

While there has been much chatter from the likes of Goldman regarding the level of wage inflation declines we’d see from a downtick in job openings or an uptick in unemployment, it’s worth considering the opposite.

If there has been significant attrition across the labor force that has led to structurally tight labor markets, will wage inflation be relatively resilient even in the face of lower job openings or even slightly higher unemployment?

This would be counter to any academic model of wage inflation but what the leisure and hospitality space illustrated after re-opening post-pandemic was that employees generally needed surprisingly sizeable wage increases - often far outpacing inflation - to get them off the sidelines and back in their jobs.

If we continue to see relatively high wage inflation as employment begins to soften in certain areas, that’ll be a deeply troubling development — signalling a level of wage inflation stickiness that isn’t priced in yet…

Wednesday: The Treasury Quarterly Refunding Announcement…

For the past few weeks I’ve been writing a little bit about treasury buybacks. Two weeks ago, it was in the context of an increasingly illiquid treasury market whereby buybacks could marginally help ease this illiquidity.

The way that this would work, mechanically, is that the treasury would buyback more illiquid off-the-run securities and issue either (by definition) on-the-run securities of an analogous maturity or more liquid and currently in-demand instruments (such as short dated bills).

Then last week I wrote that off-the-run securities that are always relatively illiquid, but have been more than usual in recent months, were catching a strong bid — a strong indication that market participants were viewing buybacks at some point as a likelihood.

This contributed, on the margins, to the loosening of financial conditions we saw through last week and was part of the reason for my concern that an announcement of future buybacks - which would immediately beat down yields in some parts of the curve - in conjunction with dovish rhetoric from the Fed would spark severe risk-on sentiment and likely loosen financial conditions even more than the week prior.

In the end, the Treasury struck the right balance in its Quarterly Refunding Statement released on November 2: saying that it would further study doing buybacks but had not made a final decision…

In addition, Treasury continues to meet with a broad variety of market participants in order to assess the costs and benefits associated with buybacks.

Treasury expects to share its findings on buybacks as part of future quarterly refundings. Treasury has not made any decision on whether or how to implement a buyback program but will provide ample notice to the public on any decisions.

It’s becoming the consensus view now that buybacks will occur. But the Treasury, perhaps with a bit of prodding by the Fed, understood that now was not the right time to announce them, especially given that treasury market liquidity improved last week as treasuries rallied across the curve.

Wednesday: The FOMC Statement…

The developments leading up to the FOMC statement took a bit of air out of the risk-on sentiment sails — with the strong JOLTS and ADP prints lending credence to the idea that the economy had not quite turned yet.

But there was no getting around the fact that the FOMC statement, released at 2:00pm, along with Powell’s press conference, starting at 2:30pm, would be the defining moments of the week — far surpassing in importance anything that came before it and anything that came after it (i.e., the non-farm payroll report on Friday).

When the FOMC statement was released, it seemed perfectly calibrated to accelerate the risk-on sentiment that had developed over the past week and a half.

In particular, the statement jettisoned the wording surrounding the high bar for stepping down the pace of hikes (i.e., sustained declines in inflation and the slowing of labor markets) that was contained in FOMC statements through the summer.

Replacing that wording was new language surrounding the need to reach sufficiently restrictive levels of rates to return to the inflation target over time, as well as the need to take into consideration the “cumulative tightening” that has already occurred.

You can read the full statement here but the most important part was the following:

In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.

The market chatter toward the end of this week was that for everyone to agree to sign off on the statement, certain members of the FOMC (i.e., likely Brainard) wanted this more dovish language included illustrating that the Fed was taking a more holistic approach to raising rates than in previous meetings.

Needless to say, unanimity isn’t a prerequisite for rate decisions. For example, within the ECB and BoE there is routinely public descents among members — as we’ve seen over the past week with both of their decisions. However, the Fed has always prized unanimity in its official communications and Powell likely thought that any dovish rhetoric in the statement could be talked down in the press conference…

Wednesday: Powell’s Presser

As Chair Powell stepped up to the podium on Wednesday at 2:30pm he had what appeared to be a nearly impossible task.

The FOMC statement released thirty minutes prior contained exactly the dovish language that the market had been anticipating. Given this, equities were rallying, yields were falling, the dollar was weakening, and credit spreads were tightening. In other words, financial conditions were continuing their trend from the week prior of getting materially looser — market participants were just waiting to make sure that Powell didn’t match the rhetoric of Jackson Hole before proceeding to rally more.

Last Friday, after markets closed, a desk note from Goldman posed the slightly snarky question of whether or not Powell was fine with how much financial conditions had eased over the preceding week.

I thought the better (less rhetorical) question was whether or not Powell fully appreciated how much financial conditions were set to ease if a dovish step-down in rates was given credence — as it’d be incredibly hard to talk down the market after endorsing the step-down unless he was prepared to do a redux of Jackson Hole.

On Wednesday at 2:30pm we found out the answer. Powell stepped to the podium and began by suggesting that a slower pace of hikes was warranted — not due to inflation having moderated but due to how elevated rates are and the cumulative impact this will have on an uncertain economy moving forward.

But just as markets began to rally further, the hammer came down. In an astonishing display throughout the course of the press conference, Powell made it clear that while the pace of hikes was likely going to slow the end destination could be higher, that no one should doubt the Fed’s resolve, and that any consideration of a pause was entirely premature.

Here are some important quotes coming out of the press conference, which you can read in full here.

Regarding the pace of hikes…

At some point, as I’ve said in the last 2 press conferences, it will become appropriate to slow the pace of increases, as we approach the level of interest rates that will be sufficiently restrictive to bring inflation down to our 2 percent goal. There is significant uncertainty around that level of interest rates. Even so, we still have some ways to go, and incoming data since our last meeting suggest that the ultimate level of interest rates will be higher than previously expected.

One of the last sentences of his opening speech before taking questions…

Restoring price stability is essential to set the stage for achieving maximum employment and stable prices in the longer run. The historical record cautions strongly against prematurely loosening policy. We will stay the course, until the job is done.

Regarding the terminal rate…

I've also said that we think that the level of rates that we estimated in September, the incoming data suggests that that's actually going to be higher and that's been the pattern.

Perhaps the most revealing part of the press conference came towards the end. After Powell had undoubtably thought that he had delivered a hawkish tone throughout the press conference (that should have prevented markets from rallying too much) he was asked the following question by Chris Rugaber of the Associated Press…

It looks like stock and bond markets are reacting positively to your announcement so far. Is that something you wanted to see? Is that a problem or what, how that might affect your future policy to see this positive reaction?

As it turns out, Rugaber hadn’t checked how markets were doing after the press conference got underway, so he was unaware that markets had already begun to fall significantly based on Powell’s unequivocally hawkish statements.

But this faux pas by Rugaber allowed everyone to see, in real time, that Powell had one goal in mind with this press conference: to ensure that financial conditions didn’t materially loosen further after nodding toward a step-down occurring.

So when he was told that he wasn’t successful, you can almost see the exasperation, frustration, and bafflement etched on his face — no doubt wondering how he could make it any more clear that there’s a certain outcome he wants (and it’s not a rally).

In his response to the question, you can see Powell trying to reframe and rephrase what he had already said — desperately trying to make it crystal clear to markets what he was trying to convey (not realizing that the markets had already got the message loud and clear).

But what was most revealing was when Powell ended his answer, shuffled a few papers in front of him, and then gave an almost post-script to his own answer. Clearly there were some talking points Powell had written down beforehand and he decided to just reiterate all of them sequentially to hopefully drill home the message…

So, okay, so I would also say it's premature to discuss pausing. And it's not something that we're thinking about, that's really not a conversation to be had now. We have a ways to go. And the last thing I'll say is that I would want people to understand our commitment to getting this done. And to not making the mistake of not doing enough or the mistake of withdrawing our strong policy and doing that too soon. So those, I control those messages and that's my job.

Note: You can watch the video of this interaction here — just skip to 38:37.

Last week, when talking about the closing of this chapter of the gilt crisis, I wrote the following regarding the delay of the fiscal statement from the end of the month to November 17 and why markets were now fine with waiting for fiscal details...

In periods of significant market stress, many mistakenly believe that what markets need is specificity as to how the stress will be resolved when in reality what is needed is a certain level of bravado: making it unequivocally clear that the right direction is going to be taken, even if the details aren’t entirely filled in at the time.

Perhaps the most obvious example of this is Mario Draghi’s famous “whatever it takes” speech that made it clear to market participants that the instability rollicking Europe at the time wouldn’t stand — and that the ECB would prevent it from continuing.

With Powell saying, “…I would want people to understand our commitment to getting this done” it’s hard not to draw parallels with the language Draghi famously used over a decade ago as he drew a line firmly in the sand.

With all that said, it was the final sentence of this answer to Rugaber that caught my eye the most. In an unscripted and slightly flummoxed moment by Powell - given how worked up he was over hearing markets were rallying, even though they weren’t - he said, “So those, I control those messages and that's my job.”

To my eyes, the best way to read Powell’s press conference is that he knew full well how the market would perceive the committee’s statement, so he wanted to make it clear that no matter what other members of the committee may think his commitment to returning inflation to target is unwavering — even in the face of potentially significant economic headwinds to come.

In other words, Powell is really saying that even if you think some other committee members may want to ease up, he’s not going to until the job is fully done, and if those other dovish committee members don’t like it then them’s the breaks.

Wednesday: The Market’s Reaction

The market reaction across asset classes could be thought of as having four distinct phases on Wednesday…

The day started with all markets trading flat with very thin liquidity as everyone waited for the FOMC statement to drop.

When the statement did drop, markets were immediately bid and risk-on sentiment was back at full steam. But after the initial surge markets went into a holding pattern waiting for the press conference before reacting any further.

As the press conference began, risk-on sentiment evaporated as quickly as it cropped up on October 21 as market participants realized that Powell had no interest in endorsing the market narrative around a step-down in rates being tantamount to any form of pivot or pause. Instead, equity markets fell as treasuries recalibrated to a higher terminal rate pushing over 500bps.

After the press conference, as market participants began to digest the implications of the press conference, equity markets continued trading down heavily as they recognized a pivot was still far off in the distance while bond markets largely stayed static.

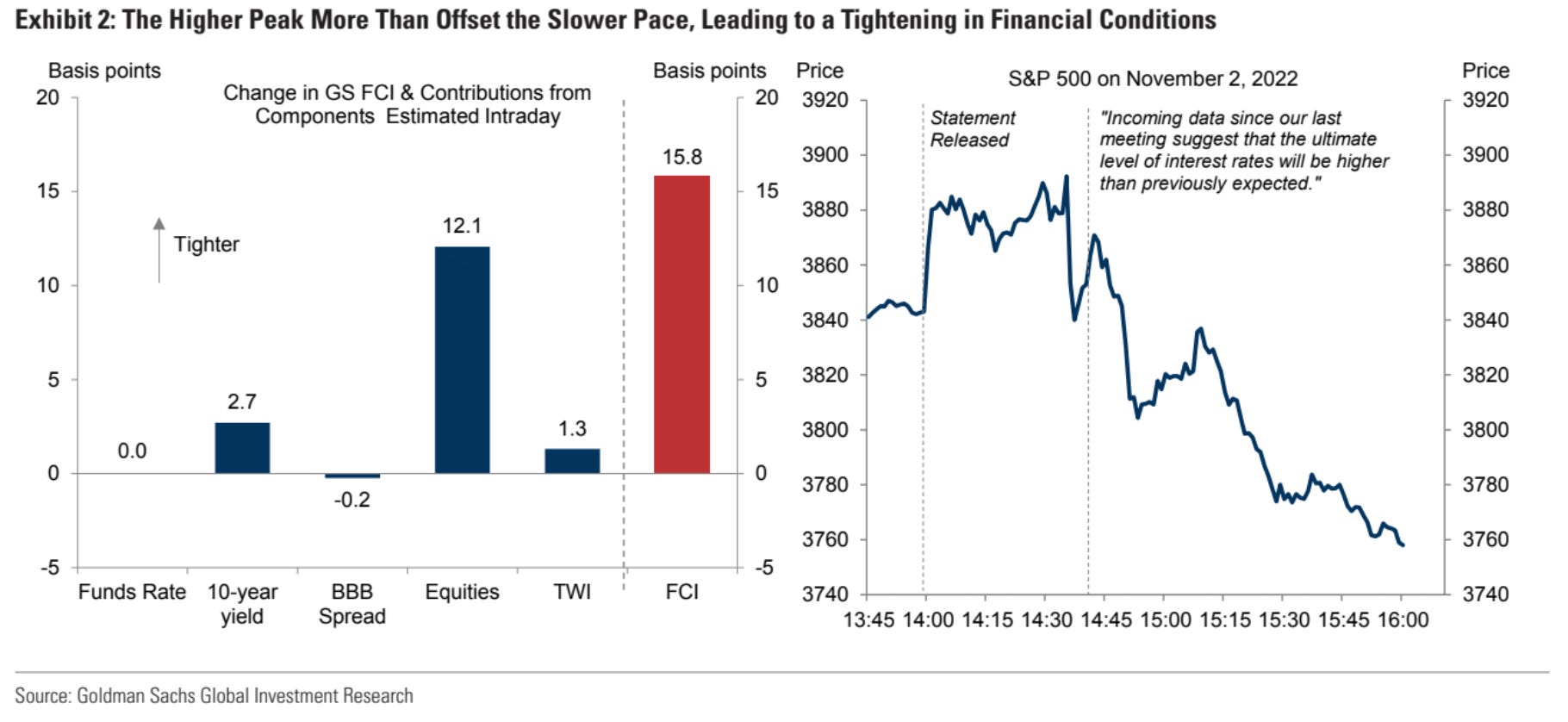

Here’s a fantastic visual from Goldman that will help you place each of these four phases, along with an illustration of what contributed toward financial conditions tightening modestly on Wednesday…

As you can see from the above graph, almost all the tightening of financial conditions came through equities falling — something that Powell would absolutely prefer, as it’s when rates or credit markets get too volatile that financial stability concerns arise.

Indeed, in retrospect what was most remarkable about Powell’s press conference was that he was able to sound hawkish enough (remember my comment about bravado!) while saying little of substance beyond that a slowing of the pace of hikes was likely appropriate (dovish!) and a higher terminal rate could be appropriate (hawkish, but something that will be informed by future data well into next year).

The “higher for longer” message mixed with the hawkish rhetoric hammered equities on Wednesday, which flowed into Thursday, but left yields relatively unscathed all else considered.

Note: By the end of the week the implied rate hike for the Dec meeting was just below 60bps — so the probability of going 75bps inched up slightly from where it was after the press conference (i.e., from a 20% to a 40% probability of 75bps).

However, in light of the statement and press conference, nearly every bank that was previously anticipating a 75bps move in December (i.e., Goldman and Barclays) have rolled back their expectations to 50bps. Here’s what GS is thinking now…

And to cap it all off, here’s a shot of where the market anticipates the terminal rate to land and how much it expects it to decline over the next year…

Turning to the world of credit, spreads for both IG and HY were even more static than rates with spreads marginally ticking up but still being below where they were prior to October 21 (i.e., HY spreads are still 20bps lower than they were two weeks ago).

The dollar whipsawed heavily between the FOMC statement and the press conference before then gaining steam through Thursday and into early Friday. But then a huge spell of weakness occurred on Friday following the mixed jobs report with the dollar ultimately falling back nearly exactly to where it was to start the week.

Threading the Needle…

Last week I argued that insofar as the Fed believes that the mechanism through which rate hikes operate is via tightening financial conditions, then it was hard to imagine how they could thread the needle of communicating a slowing of the pace of rate hikes without loosening financial conditions by feeding the risk-on sentiment pervading markets since October 21.

What made this situation all the more thorny is that this meeting was the right time to begin ratcheting down the pace of hikes. So I argued that since the statement would probably spur a rally (as it did!) then Powell’s only option to beat down the loosening of financial conditions was through repricing the December meeting (i.e., trying to leave the door open to 75bps and talk tough, as he did in Jackson Hole).

It certainly wasn’t my expectation that Powell could manage to communicate a likely step-down at the next meeting while actually tightening financial conditions solely through suggesting that a higher terminal rate could be warranted.

Because the reality is that the terminal rate is so far-dated that it struck me that trying to reprice it higher wouldn’t be taken credibly enough by markets to counterbalance the risk-on sentiment that had been building into the meeting.

This may have been partly true, because I think the real impact of the press conference came from Powell embracing what I wrote about last week and quoted earlier in this newsletter: bravado without specificity.

By rehashing every hawkish talking point he could think of - along with some phrases he had clearly penned beforehand, like “premature pause” - he was able to get the markets to backdown from loosening, all without committing to much at all.

To that end, Powell deserves a great deal of credit. Something I’ve wondered about is whether or not Powell recognized that by using bravado, without specificity, he could achieve a tightening (or at least not a loosening) of financial conditions by exclusively pushing down equity markets (since they’re more receptive to bravado, while the rates and credit markets tend to move more on specifics).

Whatever the case may be, last week I refined Goldman’s rhetorical question by asking whether or not Powell could anticipate what a dovish statement and press conference would lead to — the answer appears to be that unequivocally he did.

Ultimately, raising rates while simultaneously accepting a loosening of financial conditions only begets the need to raise rates more in the future. If you want to slow down an overheated economy, then you need to tighten financial conditions and let them stay tight — something I was heartened to see Powell explicitly acknowledge during the press conference when answering a question from Nick Timiraos of the WSJ, someone we’ve talked about before…

Very few people borrow at the short end, at the federal funds rate for example, so households and businesses, if they're very meaningfully positive interest rates all across the curve for them, credit spreads are larger so borrowing rates are significantly higher and I think financial conditions have tightened quite a bit. So, I would look at that as an important feature.

Just as I have always been quick to credit the BoE for their masterful work in the gilt intervention, I’ll be quick to credit Chair Powell for pulling off something that not many thought possible: acknowledging the slowing pace of rate hikes while managing to tighten financial conditions in real-time.

Clearly some lessons were learned about how to talk to market participants after Jackson Hole — you just have to wonder why those lessons weren’t being paid attention to back on October 21…

Part 2: Elliott Envisions Extraordinary Extremes

There are some hedge fund letters that are always worth reading if you can manage to get your hands on them — something often easier said than done. This week saw everyone clamoring to get ahold of Elliott’s letter based on a short but tantalizing FT article describing its content.

For the uninitiated, Elliott is the $55.9b AUM hedge fund founded by Paul Singer that has famously only had two down years since initiation in 1977 (they’re up 6.7% so far this year). If you’re looking for a beautifully written, albeit slightly slanted, profile of Singer, then be sure to read the 2018 New Yorker article: Paul Singer, Doomsday Investor.

The letter is 28-pages long and can be found on the “Reading List” page of Market Making alongside everything else I’ve found particularly interesting and thought-provoking this week.

But before getting into what’s contained in the letter here, it’s important to set a bit of context around Elliott — as the fund, like Singer himself, has been famously contrarian and pessimistic while achieving equity-like returns with much less volatility.