The Fed May Skip, and Goldman Has a Theory...

The wishy-washy case for skipping, revisiting wage inflation worries, and Goldman has a theory about this tech rally...

Welcome back to Market Making, your weekly dose of sell-side research and insight.

⏱️ Estimated Read Time: ~21min

✍️ Word Count: ~3,522

📚 This week’s Reading List has been updated

Part 1: Skipping, Not Pausing

It’s a reality that all members of the Fed engage in a certain level of semantic stretching — but the levels seen last Wednesday from Vice Chair nominee Jefferson rise nearly to an art form.

Jefferson commented that “…[the] decision to hold our policy rate constant at a coming meeting should not be interpreted to mean that we have reached the peak rate for this cycle. Indeed, skipping a rate hike at a coming meeting would allow the Committee to see more data before making decisions about the extent of additional policy firming.”

This sentiment has been echoed by others, like Governor Waller, too — along with the carefully workshopped use of the word “skip” to frame the now likely decision not to raise rates at the Fed’s next meeting.

Given that these were the last major comments made prior to the blackout period - where we’ll hear nothing directly from Fed members - the market reacted by rapidly squashing the pricing for a June rate hike but have nearly fully priced in a 25bps hike for the meeting thereafter (see Figure 4 below).

Some may quibble with the semantics used here: to skip a meeting is to per se pause the fastest rate hiking cycle over the past forty years. But this language was likely seen by members of the Fed as being more hawkish than just saying that a temporary pause would occur until more data comes in.

Although, as has happened many times over the past year, the Fed’s effort to dress up dovish actions in hawkish rhetoric is being seen through by the market as evidenced by JPM’s Fed Sentiment Indicator:

More broadly speaking, markets have interpreted recent commentary in a more dovish fashion, as our Fed sentiment index has declined in recent weeks, and remains near its lowest levels since the tightening cycle began in March 2022.

The backdrop to the likely pause at the upcoming meeting - or, if you insist, skip - is an odd one: it’s not so much a concern that another hike will break something, but rather that there’s an immaculate decline in inflation occurring despite the economy showing resilience — so the impetus for this decline defies a completely clean explanation.

(The obvious explanation for the lack of explanation is that the decline we’re seeing is more noise than signal — or, put another way, that we’re seeing a resetting to a still-too-high plateau and not a linear path down to target. This is exactly what’s happened in both Australia and Canada recently, both of whom prematurely paused after seeing inflation come down and economic softness emerge but who have now both raised rates again after inflation proved sticky and economic activity reversed higher).

Part of the confusion that the Fed is evidently experiencing - and why members are relatively split in their rhetoric, although they’ll almost assuredly all line up behind a pause to show unanimity after these recent comments - is that the exogenous shocks that were anticipated, that would suppress economic activity thereby doing the Fed’s job of constraining economic growth for them, simply haven’t materialized.

These exogenous shocks were supposed to come in two forms: lending contraction stemming from overall banking sector instability in the wake of the little banking “crisis” we saw last month, and the debt ceiling shenanigans of a few weeks ago.

During the last debt ceiling fight, despite a resolution ultimately being found, it led to a decidedly risk off sentiment: one that saw treasuries up, equities down, and credit spreads widen. Put another way: financial conditions tightened.

This time around market participants barely flinched in the run up to the x-date, and the whole episode is being treated as entirely in the rearview mirror. It’s almost remarkable how little of an impression it’s left anywhere in markets.

While I have my qualms with looking at the VIX to infer market stress, the fact that it’s approaching a new post-pandemic low is indicative (at least directionally) of just how much markets looked through this all…

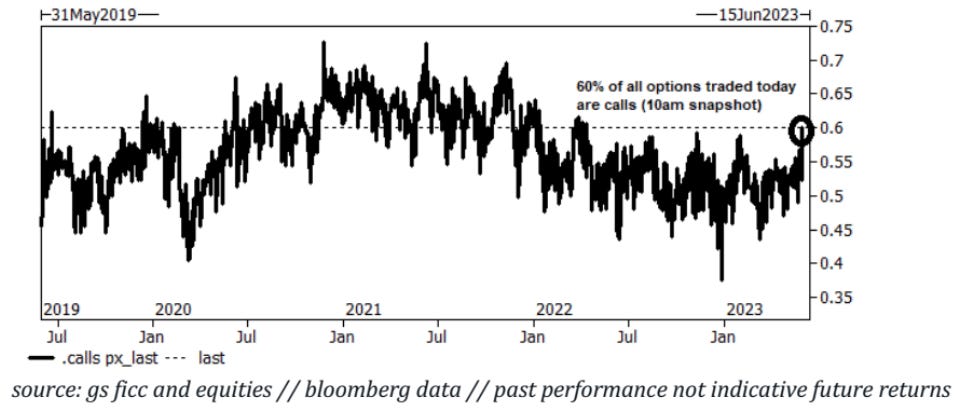

…Another way to visualize the equanimity, or perhaps ebullience, in markets right now is that over 60% of all options traded were call options earlier this week, one of the highest levels since back in the meme-filled days of 2021…

The more serious exogenous shock that many feared was supposed to come in the form of the reverberations from the regional banking “crisis” we had last month (i.e., significant lending contraction would take place across all banks thereby causing significant economic drag and voiding the need to hike rates at this meeting).

However, regional banks stocks have stabilized, deposit outflows have stabilized, lending volumes haven’t much moved, and lending surveys point to no meaningful contraction — beyond what you’d expect in a generally tighter rates environment.

Here’s how Goldman puts it…

SLOOS [the Fed’s Senior Loan Officer Opinion Survey] had already tightened significantly during the prior two quarters and worsened only slightly in the latest survey (Exhibit 9), the Dallas Fed Banking Conditions Survey was likewise already tight and showed some further tightening, the National Association of Credit Management survey showed a notable increase in rejections of credit applications, and the NFIB survey showed no increase in small business complaints about credit access.

It’s easy enough to look at the above chart from GS and notice an inconsistency: whenever SLOOS is this high, it tends to coincide with a recession.

But the view of Goldman is that this time really is different — not because there won’t be a modest contraction in credit, but because overall GDP growth will remain high enough to offset the reasonably small drag on it from this banking stress (0.4%).

And, because of this, they’ve revised down their already out-of-consensus recession probabilities from 35% back down to just 25%. As I’ve written before, this has been a contrarian view by Goldman relative to other banks, for reasons we’ll address in the next section, but it’s been directionally right thus far.

Note: These Goldman reports are contained in this week’s reading list if you want to read them — both are excellent.

When looking at the (relatively) consistent rhetoric coming out of the Fed since this tightening cycle began, it can seem like now is an odd time to (temporarily) pause: even if you narrowly slice inflation, using some of the Fed’s preferred measures like trimmed-mean PCE, we’re still well above target.

And, as Canada and Australia have just shown, a rapid deceleration in inflation can suddenly plateau, and become sticky, at levels that are still too high after pausing — thus requiring further tightening as we’ve recently seen out of both the BoC and RBA.

When paired with stronger than expected GDP data, and rate-sensitive sectors like real estate appearing to have temporarily bottomed in Q1 2023, pausing now seems to jettison the Fed’s previous rhetoric surrounding hiking until inflation is clearly on a trajectory to target. Especially with GDPNow forecasting pretty robust Q2 GDP growth and consensus estimates from market participants being revised up consistently.

To my mind, squaring this circle comes down to the Fed - having ignored real-time inflation measures that were flashing warning signs through 2021 - likely following these real-time measures more closely now (as opposed to relying exclusively on backwards looking measures like CPI, PCE, etc.).

And what some real-time measures are showing is inflation well on its way to target despite the economy still running (relatively) hot and the labor market still being (extremely) tight. When combined with leading indicators (i.e., PMIs) being soft, the Fed hinting that they’ll skip this meeting to wait for more data is likely due to hoping that these real-time indicators will begin to be reflected in the backwards looking data we get in the coming weeks.

But, as we’ve now seen in Canada and Australia, a premature pause may reinflate an otherwise deflationary path — and the longer a hiking cycle drags out, the more economic corrosion occurs just under the surface that eventually causes issue…

Part 2: Wage Gain Worries Wobble

As we’ve discussed many times before, the impetus behind Goldman’s rosier economic forecast surrounds the ability for the labor market to rebalance without a significant rise in unemployment (the latter of which historically spurs a recession even if it rises by just 1-2%).

Interlude…

I love writing about markets, and it’s been fantastic to see how many people have enjoyed reading my weekly missives. But there’s no getting around that it does take quite a bit of time to put these together for everyone each week, and my schedule doesn’t have a lot of spare time embedded in it.

Therefore, I’ve started charging a small amount for the premium version of Market Making — this premium version gives you access to the additional sections of this newsletter, along with my weekly reading list. It’s just $12 per month and you can cancel at anytime with just a few clicks.

This newsletter has always been just a little hobby and I want it to be helpful to as many people as possible, so there will always be a free section. But charging a small amount does help justify the amount of time I dedicate to it and keeps me committed to writing it even with a jam-packed schedule. So, if you enjoy my writing and want to show a little support feel free to sign up below…