Goldman Did a Poll...

Morgan Stanley and Goldman diverge on equities, Goldman keeps getting oil wrong, and the results of Goldman's monthly poll of institutional investors...

Welcome back to Market Making, your weekly dose of sell-side research and insight.

⏱️ Estimated Read Time: ~29min

✍️ Word Count: ~5,743

📚 This week’s Reading List has been updated

As mentioned last week, the Fed pausing was relatively baked in after Vice Chair nominee Jefferson’s comments prior to the blackout period.

…and with CPI not coming in hotter than expected on Tuesday, the decision to pause skip became almost fully priced in. I have plenty of thoughts on the Fed’s decision, and Chair Powell’s press conference after, but we have plenty of time to discuss the path forward, so I’ll save that for next week (or maybe do a short bonus edition of Market Making if I have time this weekend).

But it’s worth noting that the Fed did something few thought possible: paused their rate hike cycle (for now) while managing to not loosen financial conditions. This was accomplished first by the Fed raising their median expectation for rates by 50bps, along with forecasting higher growth and lower unemployment for this year…

…and by Chair Powell, in his presser, making a few relatively hawkish comments like suggesting that future rate cuts are still “a couple years out” and that “getting inflation back to 2% has a long way to go”.

In the coming days, as the dust settles, many will probably begin to view some Fed members suddenly anticipating a few more rate hikes as being more strategic than a reflection of their true views (in other words, a way for them to initiate a pause today without causing financial conditions to immediately loosen).

Either way, looking at market expectations for where rates will be in January of 2024 is instructive: we’re back to nearly where we were prior to the little banking “crisis” earlier this year (the crisis that many believed would lead to the end of this hiking cycle and usher in a new rate cutting cycle soon after).

Part 1: Goldman’s Poll Results + CPI Talk…

Goldman recently dropped the results of their latest monthly poll, running from May 31 to June 2, that got around 900 responses from institutional investors (read: some of Goldman’s clients who had a bit of time to kill earlier this month).

Let’s run through the results…

How bearish are market participants?

When it comes to risk assets, the attitude of market participants is decidedly bearish, although sentiment has improved over the past year and this month saw a reasonable uptick in neutral-to-bullish responses.

…And based on the relatively risk-on sentiment of the past few weeks, and the FOMO it has begun to engender, it’s likely that if the poll were run today the slightly bullish camp would continue gaining steam.

The driver of this bearish sentiment - as you’d expect - is the still consensus view that a recession is likely to occur within the next twelve months. Although there’s quite a large dispersion in views here with a non-trivial amount lining up around Goldman’s own view of there being just a 25% chance of a recession.

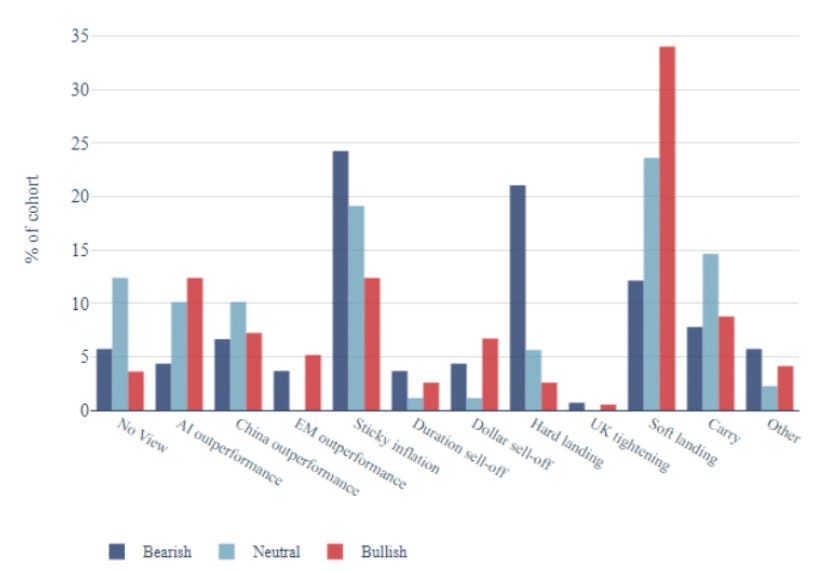

What’s the favorite theme of market participants?

It won’t come as a surprise that the favorite theme of market participants is intricately linked with their growth outlook (i.e., how likely they think a recession is to eventuate within the next year).

As a result, the three most popular themes are: sticky inflation, soft landing, and hard landing. However, in recent months the hard landing theme has fallen to just the third position and sticky inflation has gained significant momentum.

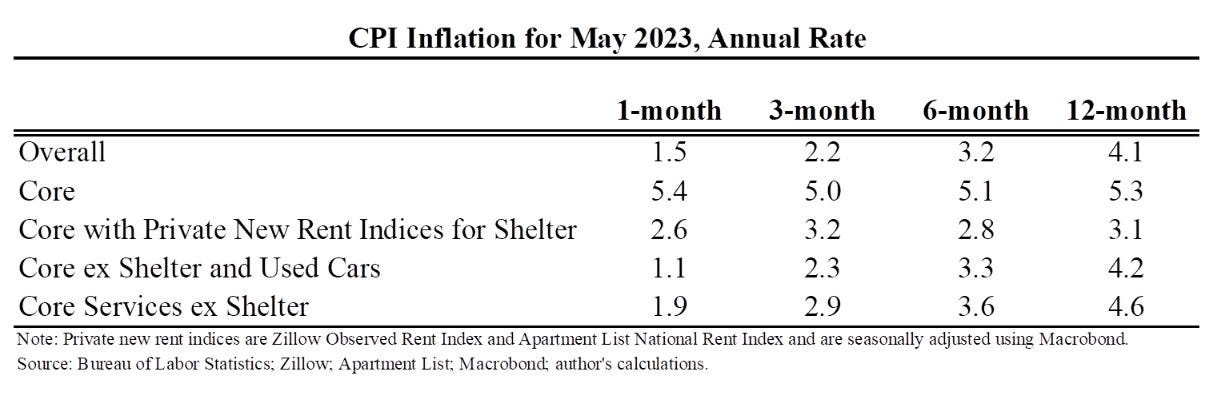

On Tuesday we got CPI that largely came inline with expectations — although core CPI did slightly beat (0.1% YoY) consensus estimates, and is showing significant stickiness at the 5% level over the past six months.

With that said, Chair Powell has been hyper-focused on core services ex. shelter, given that the primary issue in the past six months has been services inflation and shelter is inherently lagging in CPI calculations. It came in quite soft at 1.9% for a three-month average of 2.9%.

What didn’t come in as soft as many would have hoped is median inflation, which is a good way to assess just how broad-based the inflationary pressures in the system are. Jason Furman put together a great chart on this…

While equity markets weren’t overly phased, one way or the other, by the inflation print (since everything came roughly inline with expectations) in the past few weeks we’ve seen Australia and Canada, both of whom prematurely paused, restart the rate hiking engine based on the economy running hotter than expected and core remaining sticky.

…And when taking a step back, we have employment continuing to surprise to the upside, growth being revised up continually, wage inflation still running at levels incompatible with target, and core inflation remaining sticky at 5% despite the composition changing over time.

So if another month of relatively sticky core inflation comes in - along with relatively sticky wage inflation - we’ll see sticky inflation likely become the predominant theme in the next iteration of Goldman’s poll.

Note: Tuesday also had UK data deliver a shock to markets with unemployment falling and wage inflation picking back up to over 6% — which had the result of sending two-year UK yields to the highest level in ten years. The UK represents a much different (and much more difficult!) situation than the rest of the developed world is grappling with due to their rates still being nowhere near restrictive territory given how hot inflation is still running (regardless of if you look at real-time or official measures).

Anyway, it also won’t surprise you that those who are most bullish at present have a soft landing and AI outperformance as two of their favorite themes…

You may find it curious that those that are both neutral and bullish have “sticky inflation” as their second favorite theme. This all comes down to the view that sticky inflation, as long as the economy is still running hot, should allow companies to maintain their pricing power (i.e., continue to have margin expansion, or at least margin stability, just as they’ve had over the past two years).

In other words, inflation can be supportive of earnings as long as inflation doesn’t lead to a significant loss of consumer purchasing power or otherwise create margin contraction (i.e., by having costs, like wages, outpace the ability to raise prices).

Needless to say, sticky inflation and resilient earnings are incompatible over the long run as the Fed will feel compelled to continue raising rates to get inflation back down to target.

…But Goldman’s poll question was regarding your favorite theme over the next quarter, and a hot economy combined with sticky inflation can be supportive of earnings over the short term.

What’s the favorite equity index of market participants?

Perhaps not surprisingly, the S&P 500 has shot back up in recent months, and MSCI-China has fallen significantly as the China reopening trade hasn’t panned out the way most market participants had anticipated.

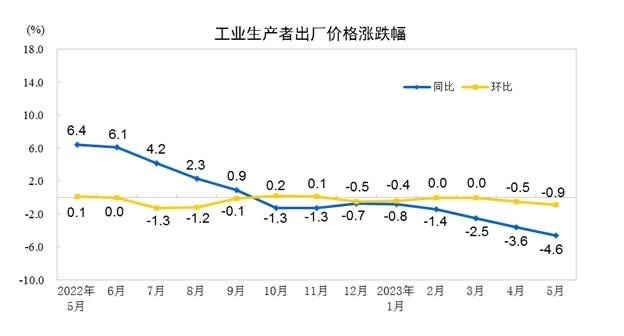

And these poll results all came before China’s (much) lower than anticipated PPI data came out…

Note: Yesterday the PBOC cut the rate for seven-day reverse repos to 1.9% from 2.0%, leading to further yuan depreciation. This has fuelled rumors that a more expansive stimulus package may be on the horizon in China.

Where do market participants see the Fed really pausing?

The Fed has taken pains to tell market participants that a skip is entirely different than a pause since, obviously, a skip denotes further tightening resuming at a later meeting.

As mentioned in last week’s newsletter, the markets took the words of the Fed at face value by almost completely pricing out a hike for today’s meeting but almost fully pricing in one for the meeting thereafter. Here’s where things stood pre-meeting:

The poll results largely reflected market pricing pre-meeting: with the majority believing that the Fed will get in just one more rate hike, and with a roughly equal divide of people thinking this skip will turn into a pause or that two more rate hikes are likely to occur.

Note: Post-meeting the dynamic has changed significantly with the market nearly fully pricing in 50bps of additional tightening over the next two meetings — so, once again, the market is revising up the anticipated terminal rate.

Lest you think that market participants in this poll were just parroting market consensus at the time they answered, the poll did reveal some contrarian takes. For example, there’s a sizeable number of participants who didn’t think the BoE would get to the terminal rate priced into markets at the time of the poll (5.5%).

This underestimation of the BoE’s resolve has been a theme for around a year now, with many simply not thinking the BoE will have the stomach to raise rates to a level that would be meaningfully restrictive in real terms (both due to the general economic weakness in the UK, and how impactful rate hikes are on households with large amounts of variable rate debt).

But given Tuesday’s news out of the UK (unemployment coming in lower than expected, and wage inflation picking back up) the BoE has much more work to do than any other developed market central bank. So, just as has happened over the past year, the BoE is likely to continue to surprise markets with just how far they go.

What are the favorite trades (long / short) of market participants?

When it comes to favored trades, there is now - just as there has been for the past year or so - a divergence driven by those anticipating a soft landing and those anticipating a hard landing.

The favored long among all market participants - as will probably come as no surprise - is being long DM bonds. This has a nice cross-current between both those expecting a hard landing and a soft landing.

The former because, in response to the economy tipping into recession, inflation will abate and the Fed will begin cutting to stimulate. The latter because the belief is that inflation is currently on track towards target and will get there before the economy tips in recession. Then, to spur economic growth from its anemic (but not recessionary) levels, the Fed will begin moderately cutting rates.

Put another way: there’s still very few anticipating the Fed going up too much from here — so there’s far more room on the downside (in yield terms) than upside. And the market is still (even after the meeting) pricing in cuts next year despite Powell suggesting they’re “a couple years out”.

Interestingly, DM equities showed a sharp rebound in this month’s results from their previous three-year low — so there’s a bit of chasing of this most recent rally occurring (even though many begrudge doing so).

As you’d expect, those most interested in equities are those solidly in the soft landing camp and those most interested in DM govie bonds are those in the hard landing camp (as the hard landing will obviously result in the most cuts occurring quickly).

Interestingly, the favored asset class of those in the sticky inflation camp is roughly split between DM equities and DM govies. There’s a bit of a timing mismatch here: if you think we’re going to have sticky inflation, that’s net negative for DM govies in the short run. But many believe that it’s net positive for the asset class over the medium term, so worth getting in on now, as sticky inflation will necessitate additional hikes which increases the likelihood of a hard landing happening eventually.

Those in the sticky inflation camp have a simpler explanation for their interest in DM equities, as already discussed above: for many corporates, assuming that they have some pricing power, inflation isn’t a bad thing in the short run (so long as the economic and employment backdrops remain relatively strong).

From the short side, there’s a bit less ambiguity in positions with DM equities still being the favored short (driven, as you’d expect, by hard landing believers, but also likely by those net long who are looking to take a bit of risk off the table).

The major change - and where many have been burnt over the past few months with bad timing - is on USD short positions. However, just as market participants have taken FX shorts off the table we’ve had a bit of USD weakness stemming from other developed markets raising rates and making hawkish squawks, just as the Fed has done the opposite (although resilient economic data has helped keep USD from falling too much over the past month).

When taken together, the two major positioning themes among the participants polled are being long govie bonds and short equities — everything else has largely reverted to being roughly flat.

And, based on the market action since the poll was conducted, you’d expect DM equity shorts, that have shown resilience as a favored short, to begin unwinding a bit more (if for no other reason than they’re getting increasingly expensive to hold).

Additionally, GS is calling out the risk of long bond positioning beginning to look pretty crowded — a good call given what happened at today’s meeting:

But, there are significant risks to bonds (and the new bullish bond consensus highlighted above makes us somewhat worried). The rates market doesn't reflect a higher for longer scenario and since we are close to 12 months away from the end of the US financial condition tightening cycle and nowhere close to target [inflation] for the Fed, another round of FCI tightener is increasingly likely.

This is a fair point and as I’ve written before the predominant consideration of the Fed, especially as it gets much closer to the end of its hiking cycle than the beginning, will be ensuring that financial conditions don’t ease too much (thereby partially unwinding the impact of having raised rates so significantly).

This will partly be done through the continued QT that’s chugging along in the background — but based on current market pricing, and the overall resilience on the employment front we discussed last week, there may be more upside risk than is currently priced in (even after today’s meeting with the upwardly revised rate forecasts).

(Plus with things like the bubble portfolio surging again, this isn’t a great omen of what’s to come vis-à-vis financial conditions tightening when the terminal rate is finally reached).

Part 2: Goldman and Morgan Stanley Diverge

Needless to say, it’s not rare that investment banks diverge in their views — but it is notable when the underlying frameworks driving their predications are wildly at odds with each other.

And that’s exactly what’s happening now between GS and MS: they have two fundamentally different philosophical views on where the economy is, how earnings will hold up this year, and what this all means for equity markets in the short term.

Mike Wilson, the Chief Equity Strategist and CIO of MS, has become the unwitting leader of those calling the recent equity rally a bear market trap and believing that equities will end the year significantly lower.

This is a rather lonely position, and one that’s only gotten lonelier this week as Goldman increased their year-end SPX target to 4,500 based on their belief that a recession will be sidestepped, and that earnings won’t meaningfully deteriorate.

To put into perspective just how divergent the views between GS and MS are: Goldman has a 2023 EPS forecast of $224 and Morgan Stanley now has a 2023 EPS forecast of $185. (The consensus forecast is $206, so both GS and MS are outliers!)

I do feel bad for Wilson because he’s laid out an interesting and nuanced framework for thinking about our current economic backdrop. But he’s become typecast as being all doom-and-gloom despite calling for 23% EPS growth in 2024.

So let’s dig into Mike Wilson’s latest note from earlier this week, and discuss why Goldman has the near opposite view.