Goldman Tries to Predict the Future...

The dominate macro themes of the year ahead, a post-mortem from JPM on last week's risk-on rally, stagflation strikes the United Kingdom, and much more...

Welcome back to Market Making, your weekly dose of sell-side research and insight.

⏱️ Estimated Read Time: ~40min

✍️ Word Count: ~8,640

📚 This week’s Reading List has been updated

Part 1: Goldman’s Themes for Next Year

Every year as the days grow shorter, the temperatures start dropping, and the snow begins falling (at least in Tahoe and Aspen), banks begin sending out long research reports on what they expect to unfold over the upcoming year.

Needless to say, it’s hard enough to prognosticate about the week ahead, never mind what will take place over the next year, so these research notes are almost invariably wrong on several fronts. For example, around this time last year the house view at Goldman was that we wouldn’t see a lift off in rates until 2023 and the word “transitory” was still being regularly invoked without irony.

But just because these research reports are almost always off-base when viewed with the benefit of hindsight, that doesn’t mean they aren’t worth reading. In fact, quite the opposite. I’ve often found these reports to be some of the best to read, because their longer time horizon necessitates more nuanced and balanced views to be expressed.

Anyway, this week Goldman dropped a few of these “year ahead” research notes, one of which covered the top ten macro themes for next year. So, I figured this would be a great opportunity to take a step back and think about some of the broader macro themes impacting markets.

But instead of walking through each of the ten macro themes highlighted by GS, I’m just going to focus in on those that I found most interesting and how we can try to connect the dots together (the full report is contained in my weekly reading list).

Before diving in, it’s worth keeping in mind that this report was released in the immediate aftermath of October’s hotter-than-expected CPI print and the ensuing risk-on rally that we discussed (in excruciating detail) in last week’s newsletter.

As a result, the report is pockmarked by some of the issues I raised last week surrounding how sensical the sudden dollar weakness is and whether the historic easing of financial conditions we’ve seen has given the Fed the permission structure not only to keep rates higher for longer, but to go higher with the terminal rate than the market currently expects.

To my mind, there will be one phrase that dominates macro discussion next year: rates divergence.

This year began with almost all developed markets having rates around the zero-lower-bound and then beginning to embark on the most aggressive rate hiking cycle of the last forty years (with the notable exception of Japan, obviously!). But now some countries are beginning to hit up against the upper limits, or what they perceive to be the upper limits, of their ability to raise rates.

Moving into next year the level of rates divergence will give way to other forms of divergence: divergence in inflation levels, divergence in economic conditions, and divergence in employment.

But let’s not get too ahead of ourselves…

Theme 1: The Narrow Path to a Softish Landing…

As we’ve talked about many times before, Goldman is forecasting just a 35% chance of a recession next year, while the median estimate is 65%. There are even some, like Bloomberg Economics, who are predicting that a recession in the upcoming year is all but guaranteed — which you have to respect, as some try to wiggle out of making any guarantees by saying there will be a 90% or 95% chance, as you can see below…

Something that gets lost when many hear that Goldman is so below consensus is that a 35% probability is still around triple what the average likelihood is of a recession in any upcoming twelve month period — so it’s not exactly like Goldman is saying the possibility of a recession is beyond the realm of reason.

The underlying rationale for Goldman’s call is that this cycle truly is different — that one of the primary contributors to our current inflationary environment (i.e., the large fiscal transfers that occurred, along with the ultra-low rates environment) also had the positive knock-on ramification of creating much more robust household and corporate balance sheets.

These stronger balance sheets will allow the economy to absorb the impact of higher rates, without tipping into recession, while giving inflation the time to slowly march down to some level approximating the Fed’s target by the end of 2023.

Put another way, if balance sheets weren’t as strong, then the impact of higher rates would be felt more immediately by households and corporates. Households would begin restraining their real spending and corporates would be doing larger scale layoffs in response to a sharp reduction in demand for their goods or services.

Goldman’s argument really boils down to being temporal: that the economy can stay stronger longer than inflation can stay higher. Whereas those who believe a recession next year is more likely than not believe the converse (with some going a step further saying that a recession is a prerequisite to getting inflation back to target).

If it sounds like Goldman is making an argument that very carefully threads the needle and somewhat goes against orthodoxy, I’d be inclined to agree. However, there are some points in its favor that are worth pointing out.

First, the Atlanta Fed’s GDPNow is predicting annualized real GDP growth of 4.2% in the fourth quarter. This is well above consensus estimates but would follow-up a relatively strong print from last quarter.

To have undertaken the fastest rate hike cycle in forty years and still have growth like this would be a strong signal that even if the economy is running on fumes next year, it may still avert a recession given that it’s starting from what appears to be such a surprisingly strong position this late into the hiking cycle.

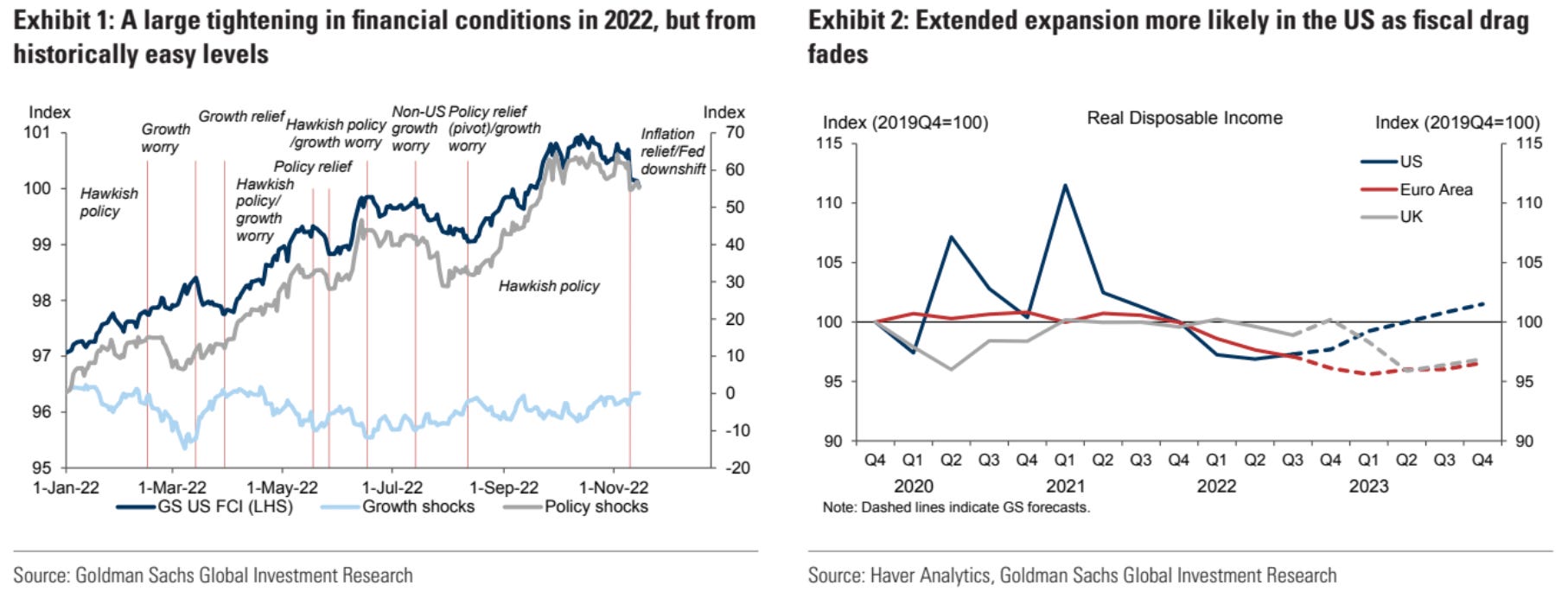

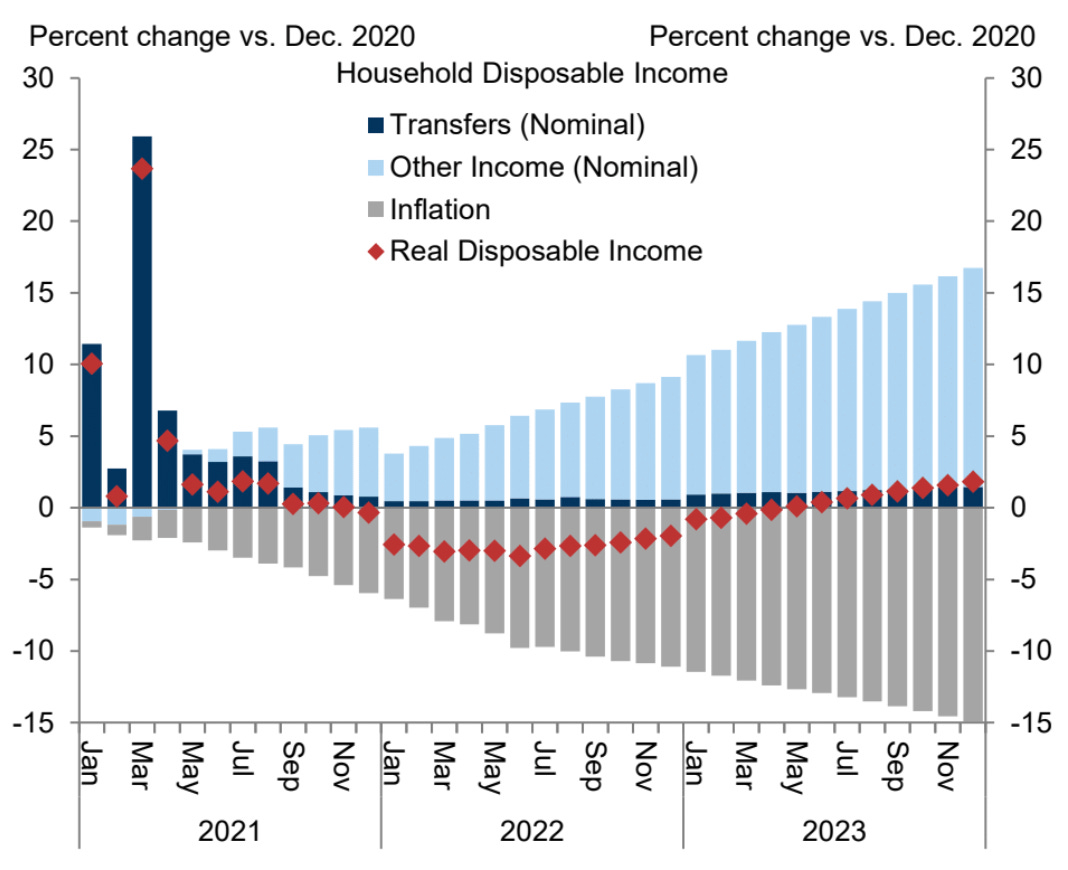

Second, per Goldman’s forecast, real disposable income will shift from being negative to being slightly positive next year as inflation begins to abate. Thereby putting households in a better position to absorb slightly higher prices, as is the case in a more normalized economic period (i.e., where disposable income goes up largely inline with the inflation rate).

While having positive real incomes is (obviously) a headwind to getting back to the inflation target, it is (obviously) a tailwind to keeping out of a recession…

Here’s another great chart, illustrating just how much households benefited from transfers just over the past few years and how inflation has eaten away at real incomes this year (which Goldman is anticipating to abate next year…).

In the end, you can think about Goldman’s argument as really being one around cycle extension: that the economy can exist in a kind of low-growth state with higher rates for the next year as inflation rolls over (due to modest reductions in demand, supply chain resolutions, much under-discussed base effects, etc.).

Then, once inflation is back closer to target toward the end of next year, the Fed can step in, just in the nick of time, to lower rates and stimulate the economy to get back to a more normalized (i.e., 2-4%) growth environment without re-stoking inflation.

Note: Goldman is anticipating just a 1% real GDP growth rate for 2023, so it’s not that they’re predicting a robust economy — like I said, they’re predicting the economy to be circling the recessionary drain, but for inflation to be squashed, and for the Fed to become more accommodative with its policy, before an actual recession occurs.

There’s a certain intuitive appeal to this line of thinking: that the economy can essentially live off of the unprecedented stimulus of the prior two years during this high rates environment until inflation is thoroughly squashed, then we can enter into a more normalized environment of modest inflation, modest real income growth, more balanced rates, and modest GDP growth — just as prevailed before the pandemic.

While this may all sounds exceptionally rosy and perhaps unlikely to eventuate, it’s largely what markets are pricing in today — especially in equities. As Goldman says…

…our benchmarking exercises generally suggest that most markets are still someway off pricing even a standard recession as their base case, and a long way off pricing a more severe recession.

As a result, we think that equities would likely still have significant downside if a full recession occurred (simple scenarios suggest from 2900 to 3500 on the S&P 500 depending on the severity of the recession…

Theme 2: Terminal Rate Upside…

In last week’s newsletter I spent a lot of time discussing the level of easing in financial conditions that occurred after last Thursday’s CPI print — which seemed appropriate given that last Thursday alone saw a level of easing that was only observed a few times before this century.

In discussing the Fed’s new reaction function to loosening financial conditions against a backdrop of potentially softer inflation, I brought up a quote from Chair Powell’s last press conference just a few weeks ago, and then said the following...

What Powell is recognizing is that not all rate hikes are created equal. Insofar as rate hikes materially tighten financial conditions and cause the entire yield curve to shift up, that does far more to restrain the real economy than, for example, the rate hike done at the last meeting has thus far.

Indeed, based on the level of financial easing we’ve seen in just the past two days you could argue that the impact of the last rate hike has been largely unwound from a real economy perspective.

But, needless to say, raising the Fed Funds rate does impact some areas of the economy directly, irrespective of overall financial conditions tightening or loosening (i.e., anything funded with very short duration, or that prices off of very short duration, so a lot of the plumbing of the financial system).

What the Fed desperately wants to avoid is a situation whereby the impact of the rate hikes already done is sufficiently unwound so as to re-inflate the economy, provide support for further inflation, and therefore necessitate re-pricing the terminal rate quite a bit higher.

To my mind, the market loosening financial conditions so significantly puts the Fed in quite a bind as any actual pause in rate hikes will beget further loosening of financial conditions — potentially undoing, from a real economy perspective, some of the hiking previously done.

So, when trying to make sense of the rates rally we saw in response to last Thursday’s CPI print last week, I wrote:

The most plausible interpretation of the significant move in rates - in conjunction with the blistering upside moves in equities and downside moves in the dollar - is that they believe the Fed will say “mission accomplished” after a few more soft inflation prints and raise rates much less than was thought just last week.

The obvious retort is that we’ve just experienced one of the strongest periods of easing in financial conditions this century, economic growth is still positive, wage inflation is well in excess of five percent and has stayed stagnant there, and the labor market is at historic levels of tightness — plus, the inflation print we just got still has annualized inflation running well north of the Fed’s target.

If you take the Fed speak that we’ve heard in the aftermath of the CPI report at face value, this much seems obvious: they want to raise rates further, but are concerned about breaking anything by doing so.

However, with financial conditions easing significantly that gives the Fed the permission structure to raise the terminal rate further, as something is less liable to break when overall financial conditions don’t seem stretched.

As I wrote last week, there’s obviously an upper-bound to just how high Fed Funds can go without breaking something in the plumbing of the financial system, and no one quite knows what that rate is.

But to prematurely pause could risk unleashing another historic level of easing in financial conditions, effectively undoing some of the cumulative rate hikes already done, and then force the Fed to (yet again) ratchet higher lest the easy financial conditions re-stoke the inflationary flames yet again.

Here’s what Goldman had to say on this, using slightly more diplomatic language…

We think that, as long as the economy avoids recession, the Fed could quite easily decide to continue gradual rate hikes further into 2023. This is partly because it may be difficult to stop tightening entirely with the unemployment rate still low and core inflation well above target.

But it is also because a non-recessionary pause to Fed hikes is likely to ease financial conditions, so if the Fed wants to keep conditions tight to maintain inflation on a downward track, further incremental hikes may then be needed.

Given this, despite the softer inflation print last week, the terminal rate base case of Goldman was revised higher to 5.00-5.25% with the final 25bps hike coming in May of 2023. The idea being that modest 25bps hikes through the first half of next year will keep a lid on financial conditions from prematurely easing…

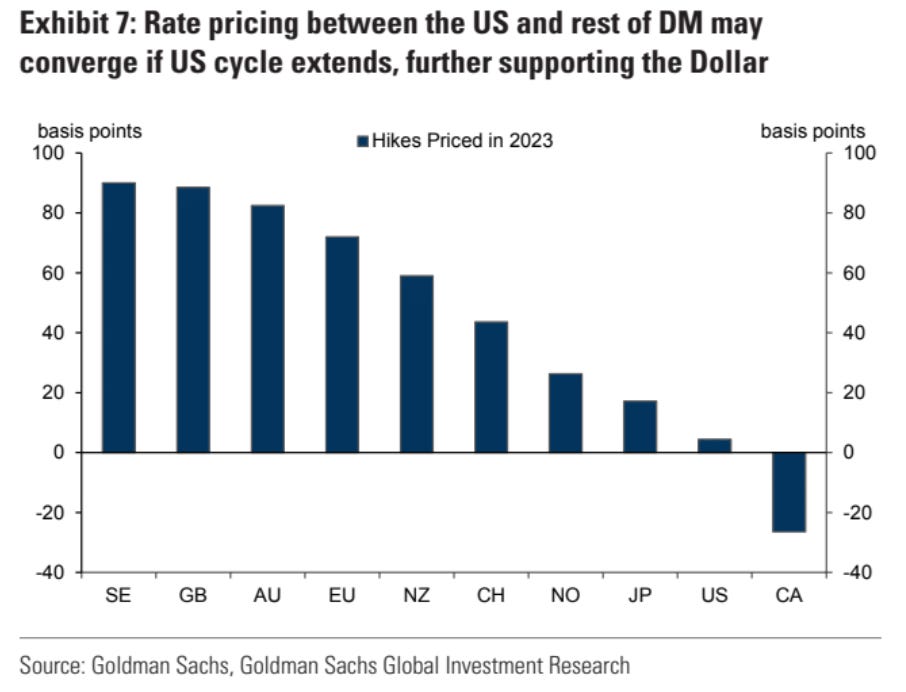

When it comes to other G10 countries, the market is currently pricing in that their central banks will almost all raise rates much more than the Fed will next year — which, on the surface, seems logical given that they largely began raising rates after the Fed had begun and have also been hiking rates by more modest increments.

The only exception to this, as you can see above, is Canada. But this is because Canada initially tried to match their rate hikes to that of the Fed in an attempt to try to insulate CAD from depreciating too much against USD — as, obviously, trying to tame inflation while contending with a depreciating currency, especially one in which most of your imports are priced, makes one’s job much more difficult.

But, as the Bank of Canada now concedes, keeping up with the Fed couldn’t be done forever — their economy, rife with over-levered households that are incredibly rate-sensitive, is approaching the upper-bound of the level of rate hikes it can absorb.

So, despite the persistent inflationary background in Canada, the BoC surprised markets with a 50bps move at the last meeting, even though the market was nearly fully pricing in a 75bps move, and has begun publicly warning of a recession arising in the ensuing quarters (echoing the rhetoric coming out of the BoE, but with slightly more subtly).

The tea leaves are being read by the market: with a recession increasingly likely and a significant percentage of households not being able to absorb higher rates for much longer, the BoC will be forced to cut rates sometime in 2023 to support the economy.

Curiously, the market seems to take for granted that even though other central banks were reluctant to raise rates as soon or as fast as the Fed (despite often having, in the case of the ECB and BoE, higher levels of inflation to deal with) that will not deter them from continuing to raise rates well into 2023 — even as the Fed moves at a snail’s pace and likely eventually pauses within the first half of next year.

This is a line of thinking I’m very skeptical of, and Goldman agrees. The market is pricing in significant future rates convergence, whereby the Fed stalls out at a lower terminal rate (right now around 475-500bps!) and other central banks catch up significantly, but to a lower terminal level, throughout next year.

However, it’s far more likely, in my view, that what we’ll see is more rates divergence through next year: whereby the Fed has room to keep raising rates at a modest level to keep a lid on financial conditions and other central banks begin to mirror the Fed’s more modest actions (i.e., not make larger rate hikes) or even prematurely pause in the face of worsening economic conditions.

Or, as Goldman puts it…

We expect those central banks to hike policy rates too, but we think the market is pricing too much tightening relative to the Fed in these markets. Risks to housing markets are higher in Australia, New Zealand, Canada and the UK, while much of Europe is heading into outright recession that also poses risks to the tightening profile that is priced.

Right now the UK is already in a recession and the BoE, as we discussed a few weeks ago, is desperately trying to convince the market it won’t raise rates as high as the market currently anticipates.

Likewise, it’s likely that Europe enters into a recession, per Goldman’s forecast, in the next year and there’s been an increasing amount of split rhetoric coming from the ECB about just how effective much higher rates will be in solving inflation.

When an economy is running hot and has tight labor markets, it’s easy to raise rates to try to tame inflation without receiving too much political pushback. However, the challenge becomes when economies begin teetering on recession and job loses begin to mount — that’s when central banks may start to blink, pause their hiking cycle, and desperately hope that the ensuing recession will wash away inflationary pressures.

That may seem like a dangerous gamble, but keep in mind that part of the reason why all central banks were so behind the curve on inflation to begin with was a concern over doing anything to turn off the growth taps.

Theme 3: Dollar Decline Doubts…

Last Thursday the dollar index saw the largest single day decline in over a decade —this capped off a period of historical weakness for the dollar, having fallen over 6% in just a few weeks.

Note: The dollar this week ended almost entirely flat — just like most markets more-or-less did after the wild bout of realized volatility we got last week.

Prior to a few weeks ago, the dollar was at levels not seen since the mid-1980s and early-2000s, so it was positioned for more downside than upside movement, but the magnitude of the downside move left many scratching their head.

Ultimately, to believe in further dollar weakness is to believe in a rates convergence story: that the rest of the world will, as we discussed above, start catching up to the Fed while the Fed pauses earlier than previously anticipated due to a softer inflationary backdrop.

Goldman isn’t buying this and does a great job explaining why, so I’ll quote them in full below:

The US Dollar still has a lot going for it. US activity and labor markets are proving resilient, and on our modal path the US economy is likely to avoid recession. However, increasing financial stability, mortgage market, and recession concerns in many other parts of the world mean that other global central banks may struggle to keep up with the Fed.

The Bank of England has been the most explicit, commenting that market pricing for the cycle may be too aggressive, but despite this, market pricing is much more restrained for the Fed in 2023 compared with others. An extended US cycle could challenge this relative pricing, further supporting the Dollar. At the same time, inflation risk in other jurisdictions compared with a resolute Fed helps to protect US purchasing power versus other currencies.

And in the event that recession concerns spread or financial stability risks materialise, this could also add to Dollar upside because of the global reserve currency’s safe haven appeal. As a result, we still see some room for Dollar strength to extend (roughly another 3% on a TWI basis).

Goldman notes that typically dollar strength peaking will coincide with troughs in economic activity, renewed equity strength, and a Fed pivoting from tightening to easing.

However, this is caveated by the fact that it may be the case that a peak in yields is a better signal of when the turn will come. Because, given how forward-looking markets now are, it will likely be the case that yields peak substantially prior to the Fed’s eventual pivot and that will mark the final peak of dollar strength this cycle.

Here’s the kind of conditions that Goldman could see a peak occurring in:

At some point in early 2023, we may see a confluence of these factors: we could be through the worst of Europe’s winter recession, a new leadership at the BoJ may gradually start to tighten policy, and China’s zero Covid policies would be on their way out, at the same time as a peak in US rates is finally coming into sight alongside some moderation of US inflation and the labor market.

It still strikes me that the easiest way to think about dollar strength comes through rates divergence: if you think we’ll have more of it than the market is currently pricing in, then we’ll hit a new peak.

But if you think that we’ll see relative convergence, whether through a more dovish Fed or more hawkish central banks elsewhere, then we’ll likely see further weakness ahead — although it’s likely that the dollar will stay higher for longer given that, in nominal terms, rates domestically will still be far above those elsewhere and be positioned against a stronger economic backdrop than most other G10 countries.

Prognosticating Problems…

Needless to say, it’s always impossible to entirely predict what themes will dominate over the next year. Certainly the level of rate hikes we’ve seen, compounded by an energy crisis in Europe, wasn’t topping the list of anyone’s report a year ago.

But while every year will present idiosyncratic challenges that no one could have possibly predicted beforehand, it strikes me that it’s nearly impossible to imagine that rates divergence will not be the dominate theme of the year ahead — or, at least, among the most dominate themes.

Indeed, when you go through all ten of Goldman’s macro themes, they all really boil down to informing rates divergence in one way or another: whether it’s China re-opening, the dollar strengthening, or emerging markets being constrained.

During times of heightened macro uncertainty, something seemingly counterintuitive ends up happening: everything begins to hinge on just one or two factors. Right now nearly all market action, when you really begin digging in deep, is being driven by rates divergence.

That’s why, in the wake of last Thursday’s CPI print, we saw significant moves in foreign equities, rates, and FX markets — it’s not that softer inflation in the US will per se mean there will be softer inflation elsewhere (inflation came in hotter than expected in the UK this past week, for example!).

But what it does mean is that the level of rates divergence will change, and that matters to markets (whether they always realize it at the time or not…).

Part 2: Wage Inflation Worries Worsen

There’s a simple reason that mostly explains why Goldman is so out of line with consensus on its recession call, and why most believe a recession will likely eventuate next year: wage inflation.

What most believe is that in order to fully break the inflationary pressures we’re seeing there simply has to be a material rise in the unemployment rate, and whenever the unemployment rate rises by more than a few percent, that’s correlated with a recession occurring.

This was a sentiment echoed by Kansas City Fed President George this week in an interview with the Wall Street Journal, saying “I’m looking at a labor market that is so tight, I don’t know how you continue to bring this level of inflation down without having some real slowing.”