Pause Without a Cause...?

The Fed creates a momentary "melt up", Goldman takes a victory lap, and markets brood over the Bank of England's bungling...

Welcome back to Market Making, your weekly dose of sell-side research and insight.

⏱️ Estimated Read Time: ~23min

✍️ Word Count: ~4,317

📚 This week’s Reading List has been updated

Part 1 / 5: The Fed Sows Skepticism

In last week’s newsletter, written in the hours after Chair Powell delivered his press conference, we quickly discussed the Fed’s decision to pause skip but let’s do a bit of a deeper dive.

Because while the Fed was trying to deliver a unified and crystal clear message, it missed the mark by a few measures as we now have Barclays calling for two more hikes, Goldman calling for one more hike, and Morgan Stanley saying this skip will turn into a true pause.

…And through Powell’s press conference markets gyrated as they tried to divine what his somewhat mixed messages meant and how they intersected with the decisively more hawkish dot plot and Summary of Economic Projections…

By the end of the day, market gyrations more or less evened themselves out across most markets (i.e., USD, SPX, etc.). But, in my email to you last week, I noted the following…

In the coming days, as the dust settles, many will probably begin to view some Fed members suddenly anticipating a few more rate hikes as being more strategic than a reflection of their true views (in other words, a way for them to initiate a pause today without causing financial conditions to immediately loosen).

Put another way, I was anticipating that market participants would eventually decide they didn’t believe the rhetoric coming out of the Fed, and that their tough talk was a transparent attempt to keep a lid on market exuberance over the Fed keeping rates unchanged.

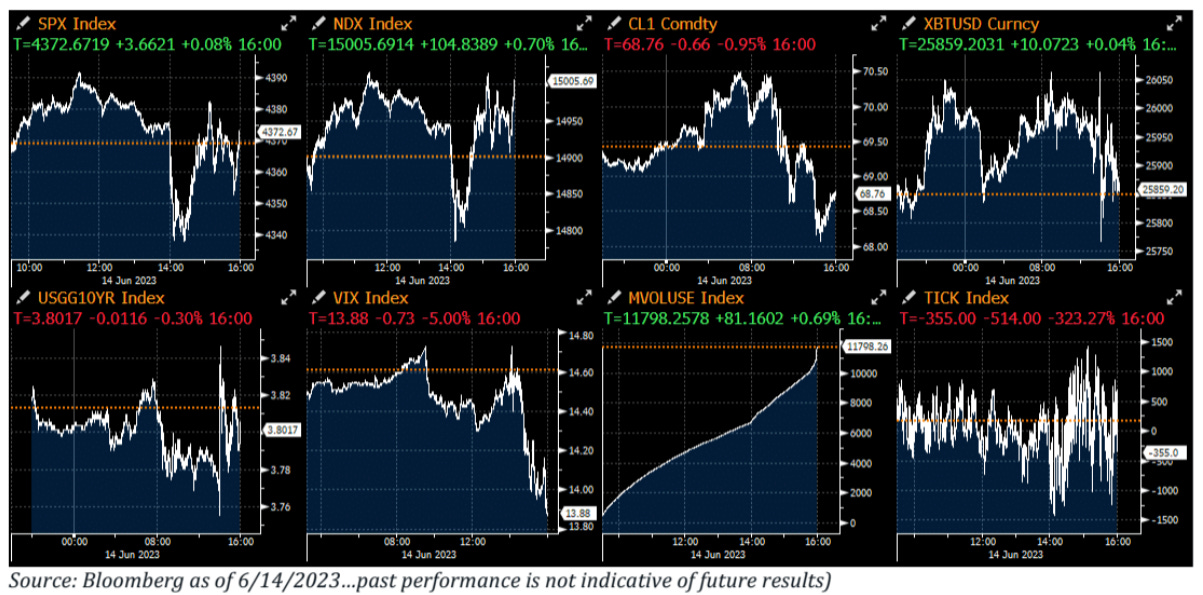

It turns out that was a reasonable (albeit not overly contrarian) take, as the next day - Thursday, the 16th - a record on SPX call option volume was set as (equity) markets coalesced around the idea that the Fed’s tough talk won’t be backed up with tough action…

Measuring how tight or loose financial conditions are is a tricky thing, and many argue over what should be included. But it’s safe to say that if you’re a central bank trying to keep financial conditions tight, and the day after you make a decision a meme-linked equities basket explodes higher, you probably haven’t achieved your objective.

Here’s a snippet from a Goldman desk note at the end of last Thursday…

MELT UP! The deluge of econ data points this morning were pretty much down the fairway (mixed overall but retail spending continues to grow and was better than feared, Philly composition was better than headline, and employment & production are increasing nicely), the market is certainly calling the Fed’s bluff and promptly buying the dips. Retail exacerbated the velocity of demand bringing the S&P to new highs, closing at 4425! Our memes basket finished at the top of the dashboard today +284bps.

And here’s how Goldman’s Financial Conditions Index (FCI) changed over the past week…

The Fed thought that through revising up their Summary of Economic Projections (SEP) they could temper the market’s enthusiasm over the Fed (temporarily?) pausing their rate hike cycle, and for a brief time it worked as the market was surprised by the sharp revisions upward.

Since Barclays made the right call on the dot plot revisions, I’ll quote them below…

The message of additional rate hikes comes out most clearly in the “dot plot” of the Summary of Economic Projections. These rate projections show a median dot of 5.625% at the end of 2023, 50bps higher than the March projections, as we had anticipated in our FOMC preview.

However, we were somewhat surprised by the extent of the support for two hikes. While in March only 7 of the participants were projecting rates above the current target range of 5.00-5.25%, today’s SEP reveals quasi-unanimous support for additional rate increases, with 16 of the 18 participates projecting at least one more 25bps rate hike and 12 of the 18 participants projecting 2 or more before the end of the year.

Notably, none of the participants anticipate a rate cut this year. This stands in sharp contrast to market expectations.

Here’s a nice little graphic of the upwardly revised economic projections and the dot plot (it was surprising to many market participants that GDP growth was revised up and unemployment was revised down so much — but these align with the allegedly more hawkish bend of participants now).

And here’s a great illustration surrounding how rate hike (or cut) odds have shifted from recent events…

In the end, as I’ve written before, the Fed is unlike most other central banks in having an almost clinical aversion to dissent — believing they need to provide a unified front, no matter what squabbles are happening behind closed doors, because this will provide markets with a clear signal as to their intentions.

The problem with this is that Fed members talk all the time. They’re always giving speeches, writing papers, and sitting down for interviews. Market participants know that there are hawks (i.e., Logan and Kashkari) along with doves, and their views aren’t exactly secrets.

In a vacuum, you’d think that the dot plot, in conjunction with the Fed’s statement last Wednesday getting unanimous support from the FOMC, would move markets quite a bit more than they did (especially when it comes to pricing for the Sept meeting) because they were unambiguously more hawkish than most anticipated.

But most market participants believe (likely for good reason!) that there was a lot of compromising going on behind the scenes: that some agreed to revise up their expectations for future rate hikes if others agreed to support the pause at this meeting and sign off on the FOMC statement.

Fed members are fond of saying that monetary policy is a blunt instrument but seem to operate under the belief that their carefully calibrates words - whether in speeches or statements - are the equivalent to neurosurgical tools. But the issue with not being earnest, even if it’s at odds with other members, is that the market will simply default to trying to read the tea leaves as opposed to taking what you say at face value.

Barclays is calling, as mentioned earlier, for the Fed to hike another 25bps in July and then again in September to 5.50-5.75% (based on an expectation of real GDP coming in hotter than expected, and the labor market staying tight).

Interestingly, they do raise the prospect of the September meeting being skipped, just as this past one has been, to be replaced with a hike in November — so they’re calling for the Fed to possibly move from a 25bps-per-meeting stance to a “skip-every-other-meeting” stance until they hit their terminal rate.

Part 2 / 5: Goldman Calls Out Inflation Optimism

Goldman is currently only calling for a July hike. But, if there are going to be two more hikes, believes they’ll come in July and November — with the Fed skipping September in the hopes that favorable data comes in before then that obviates the need to go in November…