Soft Landing Hope Rises

CPI cools and markets drool, Morgan Stanley finds hope in a soft place, and an important update...

Welcome back to Market Making, your weekly dose of sell-side research and insight.

⏱️ Estimated Read Time: ~21min

✍️ Word Count: ~4,066

📚 This week’s Reading List has been updated

Part 1: CPI Cools, Markets Drool

There was no question that today’s CPI print would come in soft relative to recent months — the only question was how soft it would be. To this end, banks seemed to be engaged in a game of limbo in recent weeks beating down their estimates of how low headline and core would come in.

And yet even with this game of limbo playing out, the results still surprised to the downside…

There are many notable numbers here, but core coming in so soft is no doubt the biggest surprise as it’s the smallest increase we’ve seen since February of 2021 (driven by airfare declines, along with shelter and used cars churning down).

Immediately upon headline and core data being released, markets reacted with equities flying and yields plunging (after the latter increased steadily over the prior week)…

While there’s no getting around that this is a good print by nearly any measure, it doesn’t exist in a vacuum. And under the hood there is a bit more of a mixed picture. The core downside surprise was driven primarily by known factors (i.e., shelter and used cars) along with the surprise of airfare pulling back 8.1%. But wage-sensitive categories such as car repair (+1.3%) and physician services (+0.7%) showed resilience.

With new car prices stabilizing, rents beginning to flatline or tick up in certain geographies, oil hitting $80/bbl partly due to dollar weakness, and risk assets being bid up in a redux of 2021 the relatively linear path that inflation has fluttered down will begin to get messier moving forward.

This is partly why, despite the below consensus read today, market pricing of the Fed’s next meeting barely budged with 25bps still nearly being fully priced in. GS, in a modest victory lap, reiterated their call that after raising by 25bps at the next meeting the Fed will have reached its terminal rate. But it’ll be some days before we see if others begin revising down their two additional 25bp hike calls (i.e., BofA).

In these last innings of the rate hike cycle - and there’s no doubt that’s where we find ourselves, regardless of if there’s 25bps or 50bps or even 75bps more of tightening to come - the Fed will find itself in an increasingly sticky situation.

As we’ve discussed before, the rapid rate hike cycle spooked many but real rates were still decidedly negative until recently. Now, with inflation getting closer to target and Fed Funds being over 5%, we’re in restrictive territory (here’s a good piece from the Kansas City Fed discussing restrictive rates recently).

So, on the one hand we do have restrictive rates, but on the other we have GDP growth being revised up, real wages surging based on continued wage inflation with a more limited price inflation backdrop, real spending ticking up, personal savings rates stabilizing, and financial conditions loosening based on the euphoria surrounding getting (close) to the terminal rate with nothing having broken (yet).

This is a recipe, that we’ll discuss shortly, that some (i.e., Morgan Stanley’s chief US economist) believe is consistent with a soft landing, whereas many others see this as a recipe for inflationary pressures reemerging — or something unpredictable breaking (see the BofA commentary I put together with the MS commentary below).

Overall, the economic backdrop - in the US, at least - remains relatively healthy, albeit much reduced from Q3 or Q4 2021…

If you’ve read my writing for long enough, you know that financial conditions are one of the things I pay most attention to despite how much one can argue about how to define financial conditions tightening or loosening.

Here’s where financial conditions are today, and how they changed in the week prior to today’s print (with today’s CPI print, financial conditions have loosened significantly and they’re already in relatively loose territory).

Part 2: Goldman’s Latest Poll Results

Last month we discussed Goldman’s poll of around 900 institutional investors (i.e., GS clients who have some time to kill, so actually respond to the poll) that they run monthly.

Today (July 12) Goldman sent out the latest results of their poll, run between July 4 and July 6, that has some interesting results: the hard-landing theme has remained relatively resilient despite recent market action (with market participants not revising their recession calls, but merely pushing out the start date) and bearish sentiment prevails.

We talked last month about the poll results being roughly inline with market pricing, as you’d kind of expect if you’re polling a pretty wide swath of (very large and very active) market participants. But this month is a bit different: the soft landing now firmly baked into equity pricing is being ignored and those polled anticipate the ECB will go further than the market is currently pricing. So there’s some contrarianism afoot.

Sentiment on risk assets and recession probabilities…

The last time we talked about the poll results coming out of 200 West, I said that intervening data (i.e., cooler inflation than expected, rising equity markets, etc.) would almost certainly turn sentiment noticeably around as market participants began to “buy in” to the price action flickering across their screens daily.

Well, there’s certainly rally chasing happening in markets these days — but apparently the vast majority are still loathe to do it. Sentiment barely changed month-to-month, despite the data we’ve received over the past month being nearly uniformly rosy.

This is perhaps sensical when viewed against the backdrop of what’s being viewed as the primary risk-on or off drivers — with overall economic growth, not monetary policy, clearly the predominate consideration. (Everyone has become slightly accustomed to elevated rates — and, as we’ll discuss in a BofA snippet shortly, this is relatively normal in the last phases of a rate hike cycle).

And the sentiment around a recession eventuating isn’t much changed from not only last month but in late last year when yields rocketed higher and equities plumbed new depths. The only difference is that folks are now projecting a recession to start later…

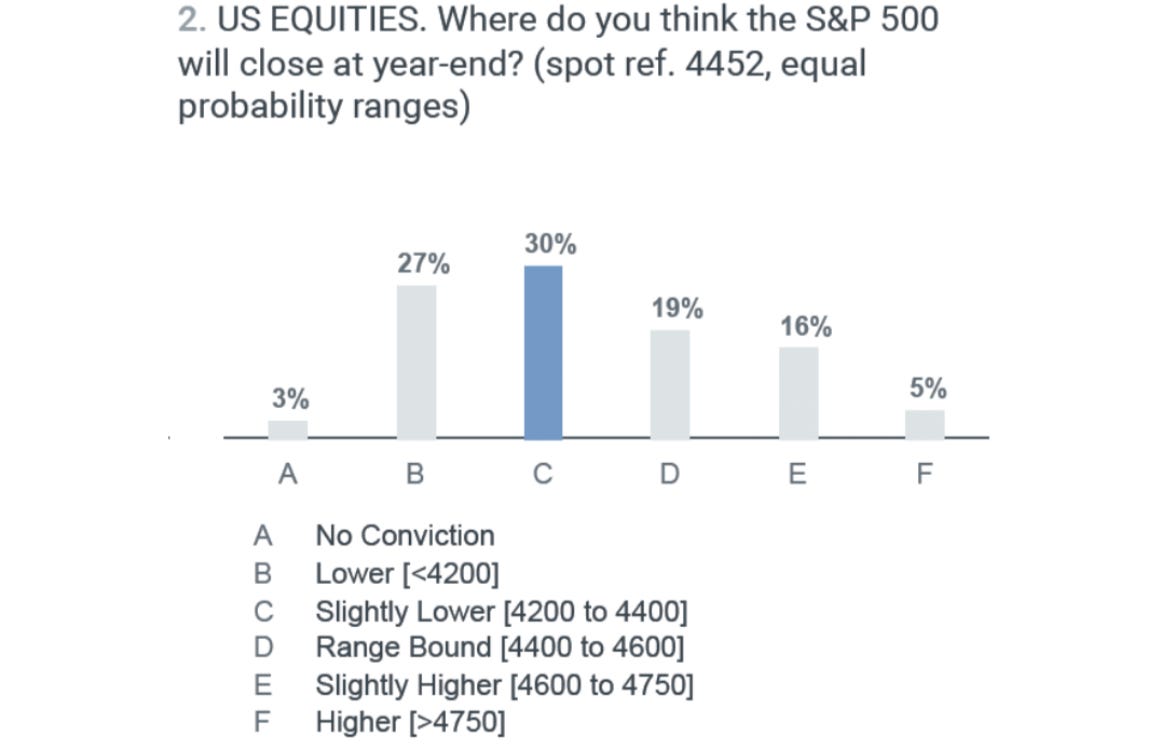

Equities enthusiasm not building (yet)…

It’s not atypical to see folks hate a rally until the latter stages of it, but its notable just how much disdain this rather sharp rally - in conjunction with the softer data we’ve received - is getting.

Fully 57% of market participants think equities will end this year lower, with only 21% seeing this rally having more steam. So, when it comes to the “catch-up” issue we discussed several weeks ago regarding market breadth, not many are buying it.

Note: A desk note from GS in the aftermath of the print painted a different picture, anticipating large inflows coming and pitching going into more equal weight indicies to capture the “catch up” to come…

I am bullish for the rest of July as remaining macro shorts get covered and investors move from the sidelines back into risk assets. R.I.N.O market = recession in name only. There is a $5 trillion “wedge” between Money Market Funds and bonds vs. equities. Bad Breath No Longer… Got Listerine? If you have not already added RSP (SPX Equal) or QQQE (NDX Equal) to your radar, now is a good time. The flows are swarming here.

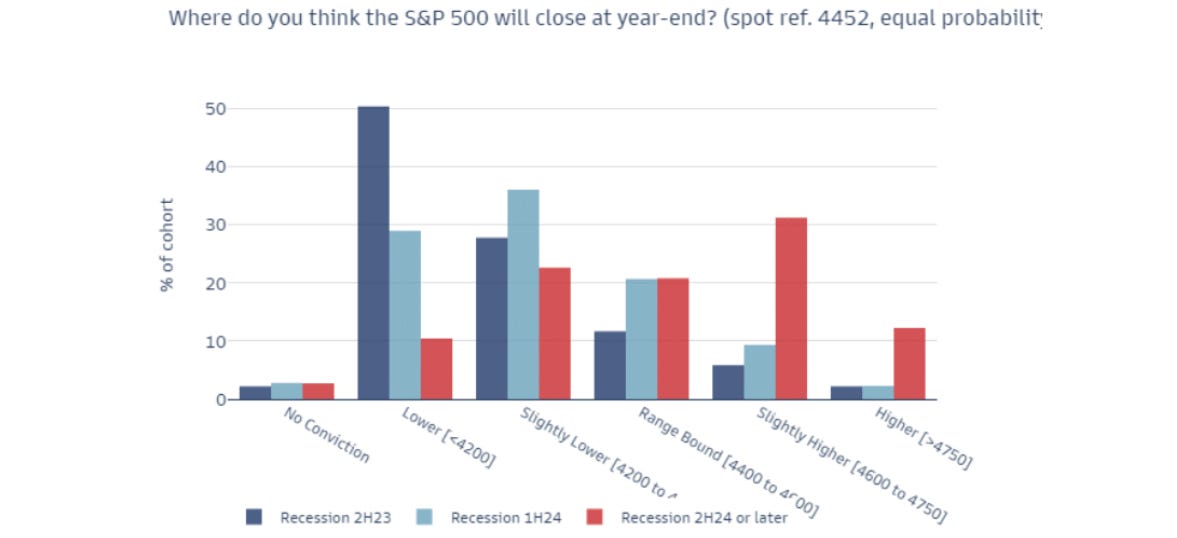

However, as we discussed the last time the poll was run, one needs to really disentangle recessionary-views to get a meaningful read on equity positioning. Because there’s a clear divide with those calling for a recession having very bearish views. So if the tide begins to turn more toward a soft landing consensus you’ll see positioning, and sentiment, change rapidly on risk assets (especially equities).

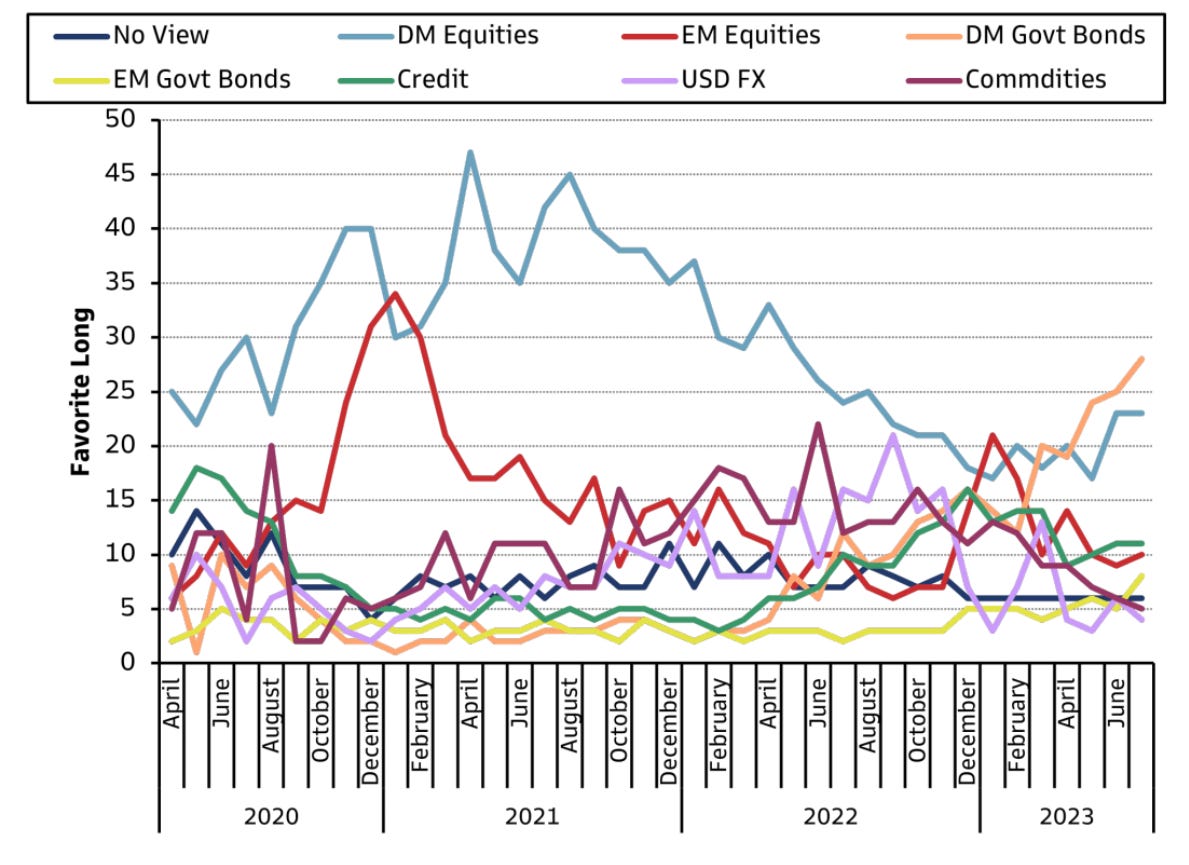

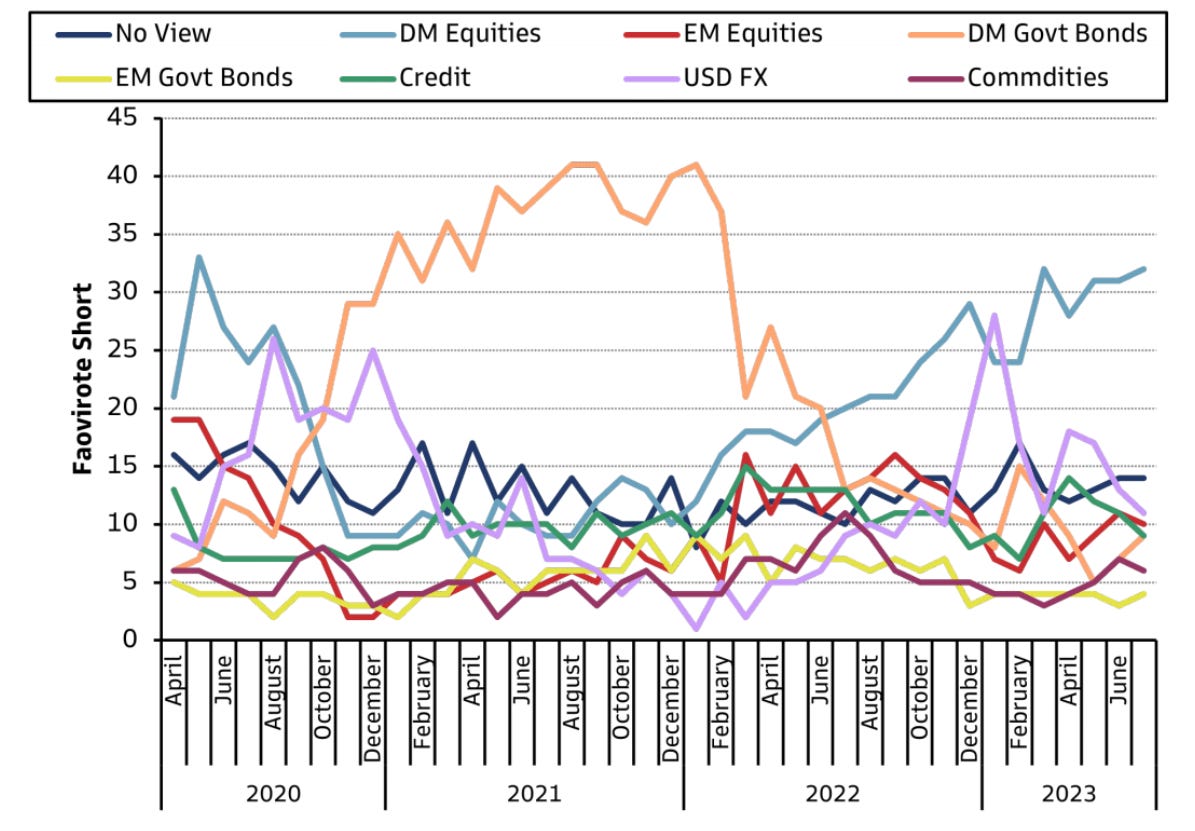

Asset allocation views…

When it comes to asset allocation, it’s much the same: favorite net longs are DM Govie Bonds and DM equities (with those viewing a recession as unlikely driving this position), while favorite net shorts are decidedly DM equities (with those viewing a recession as likely driving this position).

When taken together, positioning is net flat with one major exception: DM govie bonds. And the rationale here is simple: most market participants are positioning based on their views of a recession.

If a recession does eventuate in the next twelve months, then one would expect rates to come down relatively quickly as there are exceptionally few who think a recession, and the commensurate rise in unemployment, won’t bring inflation back to target, or temporarily below target, and keep it there.

If a recession doesn’t eventuate, but rather a soft landing occurs, those in that camp believe that the Fed, seeking to stimulate potentially sluggish growth with inflationary pressures (mostly) in the rearview mirror, will lower rates slightly from their increasingly restrictive (in real terms) levels.

Put another way: whether you’re long or short any given asset today will likely hinge largely on your view of a recession occurring, but given how elevated rates currently are there’s an interesting confluence when it comes to DM govie bonds. Everyone thinks they’ll come down in the next year — they just disagree on why.

Europe and China…

In discussing last month’s poll it was noted that the market was, yet again, heavily underpricing how much the Bank of England would be forced to move (in fact, the views of those polled were even below current market pricing).

The opposite is true regarding the ECB, with those polled seeing more upside to the terminal rate of the ECB than is currently priced into markets.

As you’d expect, most polled don’t have an outright view on the Renminbi. But with weaker than expected growth numbers, housing instability remaining an issue, and manufacturing data sluggish, there’s increasing consensus around USDCNH weakening from the current 7.22 level.

Part 3: Morgan Stanley Mulls Over Soft Landing

We’ve talked quite a few times before about Mike Wilson over at Morgan Stanley and his widely misunderstood call surrounding an earnings recession to close out this year, followed by a resurgence in earnings next year.

Many have conflated Wilson’s call on earnings with his call on the broader economy. But this isn’t quite fair, as he’s waffled a bit on his overall economic outlook and doesn’t view the two as necessarily being intertwined (for reasons we’ve talked significantly about regarding elevated inventory and poor operating leverage).

However, there’s no getting around the fact that he’s anticipating significantly more economic weakness than some of his colleagues are. Because Zentner, the chief US economist at MS, has a new piece out calling for a soft landing — and, much like Wilson is staunch in his earnings call, Zentner is staunch in her economic call.

It’s an old saying that central banks are always fighting the last battle. In other words, they over-index on the lessons learned from their last fight, sometimes forgetting lessons learned from many fights before.

Similarly, the central contention of Zentner is that companies will over-index on the lessons they learned from the pandemic (i.e., that you shouldn’t be too quick to lay off people, because the economy may bounce back quickly and you may have trouble rehiring).

So, per Zentner, the labor market will stay just tight enough to keep out of recession, even if economic growth slows substantially, while simultaneously being loose enough to allow inflation to churn down with real wages staying positive (thereby stimulating the economy a bit, but not too much).

Here’s exactly how Zentner puts it…

Hard landings are recessions, that is, periods of declining economic activity that trigger dislocations in labor markets, causing upswings in unemployment rates and negative payroll prints. They are hard because the economy enters a vicious cycle in which depressed aggregate demand causes layoffs, reducing labor income which magnifies the intimal drop in demand. Our call for a soft landing is underpinned by a labor market that slows but remains resilient as companies in certain sectors continue to backfill positions, as well as retain existing workers.

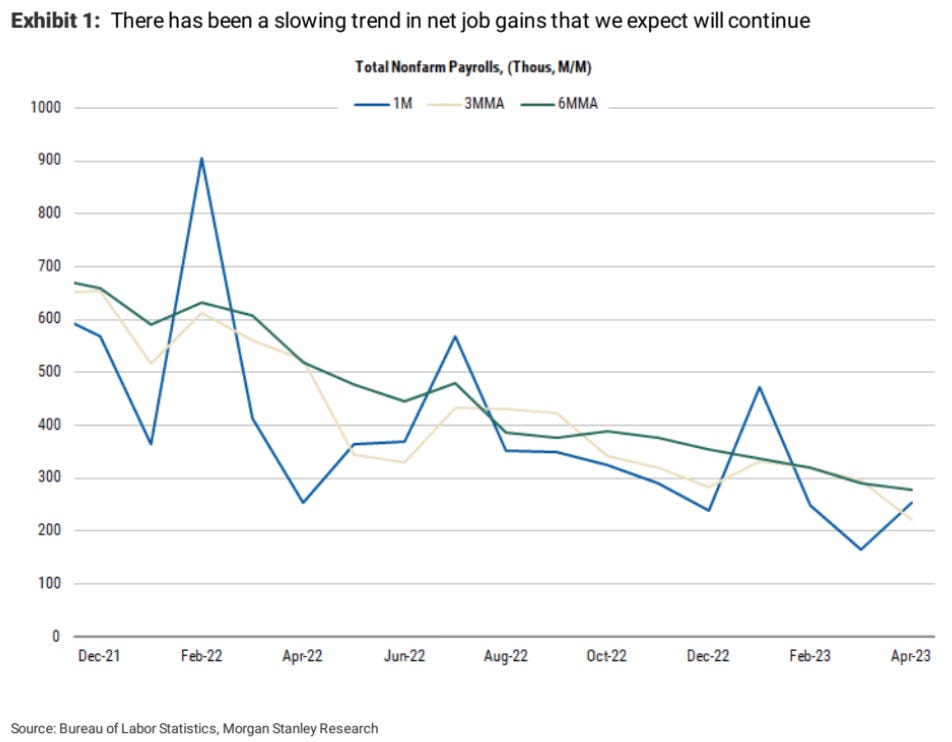

There has been a clear deceleration in payroll numbers since 2021 despite recent strong print. The 6-month moving average has been decreasing at a steady pace since 2021, and we project nonfarm payrolls to fall below the 90,000 replacement rate in 4Q23 and remain there through most of 2024.

However, we think the US economy is likely to skirt a recession. We project the economy cools further but avoids a hard landing in large part due to labor market resilience. What gives us the conviction for our call? In this note, we highlight key points on the US labor market supporting the soft-landing narrative and detail what data we are following closely to determine if the economy indeed remains on the soft-landing path.

Like all soft landing arguments, there’s a lot of linkages that need to hold under stress. But, based on the data we’ve been getting in recent months, including today’s CPI print, a soft landing is becoming more and more probable.

Let’s briefly go through the key arguments here…

#1: The economy is still understaffed…

Given the robust payroll prints we’ve been getting for months - even with last week’s softer number that was still well above the replacement rate thus partly why the unemployment rate ticked down - it can be hard to imagine that the economy is actually understaffed.

However, Zentner points to the historical relationship between payrolls and GDP growth (Okun’s law), and based on current GDP growth finds that payrolls should be 300k higher in aggregate than the current level.

If that seems slightly too academic, you can also look at a measure like GDP per worker and what you’ll find is that we’re still significantly above trend which, again, suggests we’re probably understaffed — at least in parts of the economy.

The more intuitive way to think about understaffing is simply that in a more normalized (i.e., pre-pandemic) economy, during times of relatively flat growth you tend to see sector rotations (i.e., layoffs in manufacturing but growth in employment in service industries, etc.).

Key to Zentner’s argument is that we have a real, structural undersupply in certain service sectors, that collectively make up 1/3 of private employment, and that we’re likely not going to see any meaningful sector rotation because sectors that are currently under more strain (i.e., manufacturing) will be hoarding more labor (i.e., willing to suffer short term losses out of fear of not being able to re-hire when the economy gets going into motion again).

#2: Backfilling and hoarding…

An interesting argument made by Zentner is that even if you believe that private payrolls are going to fall significantly (i.e., there’s no real understaffing occurring, and private hiring will cool) there’s one major sector of the economy that still has lots of catching up to do: the public sector.

In general, government payrolls tend to ebb and flow with budgets, and with the pandemic there was wide shed state and local layoffs. Even with relatively healthy inflows over the past few years, the gears of government grind slowly and it often takes years for them to begin hiring again.

As the below illustrates, government payrolls have been slowly expanding to fill in the “gap” caused by the pandemic — but they’re still lagging far below trend. And with economic activity, and government coffers, being in a relatively healthy position since they’re impacted most by their local unemployment rate, there’s little reason to anticipate this gap won’t continue to be filled.

As mentioned earlier, labor hoarding has been a dominate theme for a few years now, with companies not wanting to repeat the cost and headache of hiring new employees that they suffered through 2021-2022.

Zentner believes we’re already seeing labor hoarding, and there’s no reason to think we’ll see any less moving forward unless we begin seeing significant economic weakness.

For example, GDP per worker in non-understaffed industries (although there’s some subjectivity in what industries are understaffed) has dipped into negative territory without there being widespread layoffs in these industries…

Labor hoarding suggest a significant jump in layoffs can be avoided, and so far the data have been aligned with our call. [Below] shows that while hiring rates have been decreasing since 2022, private layoffs remain below pre-COVID levels and close to historical lows (layoffs data start in 2000). Layoffs have been concentrated in a few sectors, predominately in tech, which reflects more idiosyncratic factors than broader macro trends. Tech, which represents less than 1.5% of total payrolls, over-hired in 2021, surpassing pre-COVID levels, and we interpret recent layoffs as a correction towards historical trends.

#3: Higher participation rate will ease inflationary pressures…

Something we’ve talked about many times is that the key to getting inflation back down to target - and having it stay there - is getting wage inflation back to a level that’s consistent with target (around 3-3.5%, depending on who you ask). (Usually we’ve discussed this in relation to Goldman’s wage inflation theory).

Zentner thinks that given the wage increases that have already occurred, it will begin to entice more and more workers currently on the sidelines to get into the labor force (increasing the supply of workers thereby reducing overall wage pressures moving forward).

There are signs that this is what’s happening now, as prime age workers (25-54) have a participation rate now above pre-pandemic levels with room to grow further, and there are other groups still behind where they were pre-pandemic (so there is room for the participation rate to nudge up, as people get drawn in by the level of current wages, irrespective of future increases to that level).

An increase in the supply of workers should be interpreted as a positive supply shock, that is, as an increase in production capacity or potential GDP. More capacity means higher economic growth, and a better balance between demand and supply of goods and services, which helps to mitigate inflationary pressures. Moreover, more labor supply implied less wage inflation ahead and as a result, lower core services ex-shelter inflation.

#4: Moderating wage growth will support demand without inflaming inflation…

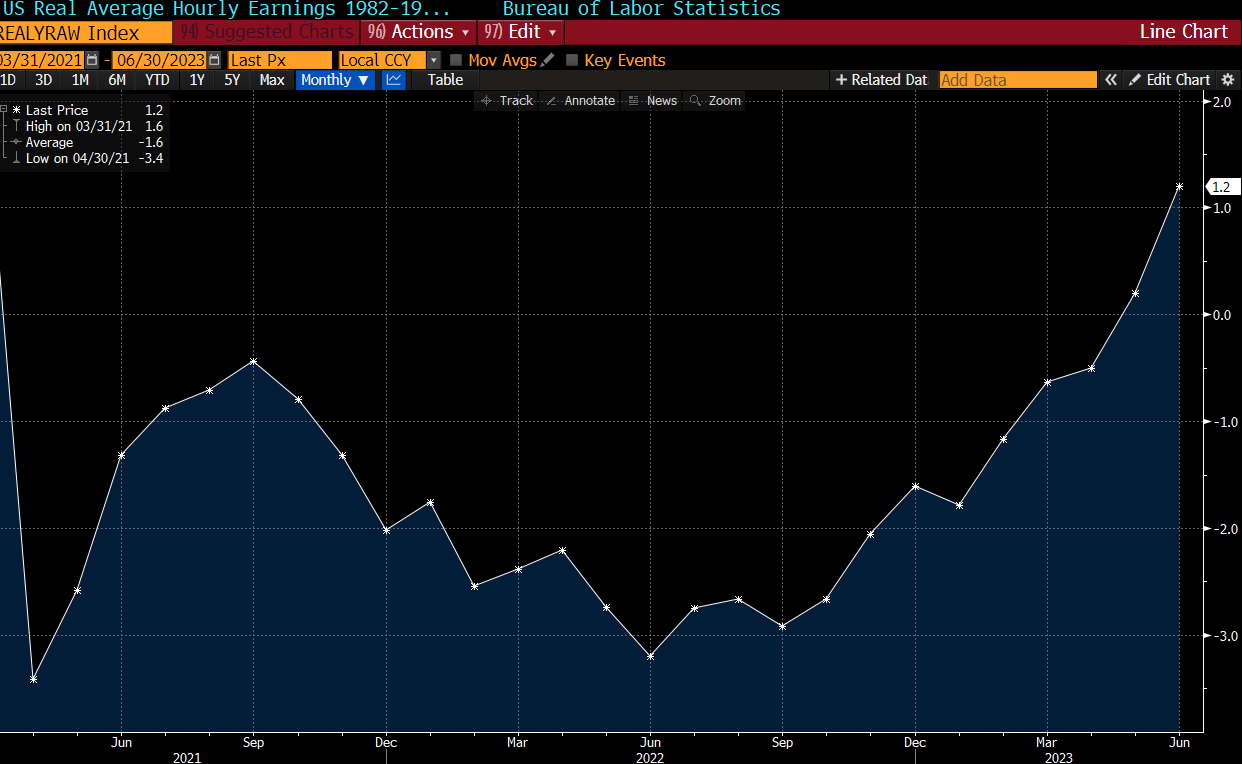

The final point by Zentner is the one where most will quibble. The basic argument here being that with headline CPI cooling, and wage growth suddenly turning positive, that’ll put less pressure on workers to demand outsized wages.

In other words, if you feel like you’re falling further and further behind because you got a 5% wage increase, but inflation is running at 8%, you’ll agitate for an even larger wage increase (thereby, in theory, spurring something looking like a wage-price spiral).

But if inflation is at 4% and you get a 5% wage increase you won’t necessarily be agitating for a much higher increase. So, the thinking of MS here is that wage inflation will continue to moderate, and this will feed into inflation moderating.

However, the important point made by Zentner is that you want wage inflation to moderate gradually, and for real wages to be flat or slightly positive, so that consumers keep up their level of spending (because if they cut back significantly, then that’ll obviously feed back into declining economic growth and put downward pressure on the labor market). So you want both wage inflation and price inflation to enter into a kind of positive tailspin together — just not too quickly that layoffs begin occurring or that you get deflationary pressures arising.

The question here then is how will inflation moderate back down to target in this scenario, and the answer (not stated by MS, but implied) is that the Fed would prefer to have the economy sluggishly moving along at elevated levels of wage and price inflation as long as both are feeding on each other and fluttering down (slowly).

The issue is that this leaves open the possibility of rates needing to be maintained at restrictive levels and, eventually, something may break or, perhaps worse, inflationary pressures may once again build due to some idiosyncratic reason (i.e., an oil shock occurring, something that Jeff Currie at GS may like to see so his higher oil calls are finally vindicated!).

The Fed recognizes that the longer rates stay at elevated levels, the more wobbly something is going to get. Crises often come from places you’d least expect them. Despite the credo of “higher for longer” gaining steam, the Fed would ideally like to have an excuse to begin cutting sooner rather than later.

But, if MS is right, then they’ll have no excuse to do anything other than keep rates elevated for longer with payrolls continuing to grow while wage and price inflation march slowly downwards. Premature pauses are one thing, but premature cuts are verboten.

Here’s a little snippet from Bank of America discussing this, and splashing some cold water on those calling a perhaps premature victory…

So the rates are back in play in a big way: the 10yr UST back over 4% for the first time since Feb; the 2yr touched on 5.12%-the highest level since June 2007.In the UK, the10yr has breached 4.64% level–the peak achieved during the LDI crisis last Oct. The rate risk is back as the front and center driver of volatility in credit.

Our core view here remains that the full extent of damage from tight monetary policy is unknown until the peak in policy tightening is behind us. We are clearly not at that point yet. Exhibit 1 shows have every single episode of a local peak in UST 2yr yield was followed by some risk-negative event over the past 40 years. Such episodes ranged from mild (Mexican peso crisis in Dec 1995; HY +95bp) to moderate (Asia FX crisis in Oct1997; HY +350bp) to severe (GFC; HY all-time wides). The lag between the peak in 2yr yield and subsequent event varies from just a couple of weeks to just over a year, with an average being 7 months (Exhibit 2). It is rare to have an indicator that works every single time; this is one of those rare instances.

Part 4: Market Making Update

I love writing about markets, and it’s been incredibly rewarding to see how many people have enjoyed reading through the newsletter each Wednesday. I know that many have used my writing to help stand out in interviews, or during their current summer stint in sales and trading, which is really heartwarming.

However, in recent weeks my schedule has started to balloon and, obviously, my actual work needs to take priority over this little hobby of writing thousands of words on market themes each week.

As a result, the Market Making newsletter will no longer (sadly) be published each Wednesday. Instead, whenever I have more free time to sit down and write, I’ll send out a note going over my thoughts on what’s happening. But it’ll be far less frequent.

This newsletter was always designed to try to help, so hopefully you’ve found some value in the editions that have come before this and hopefully you aren’t too disappointed with it ending!

For premium members of the newsletter, all subscriptions have been permanently paused to ensure that no one is charged moving forward. However, you should still have full access to the archives, past reading lists, etc. even though your subscription is permanently paused.

For those few who opted for the annual subscription, I’ve already processed a full refund for you. For those on the monthly plan (that’s now paused, so you won’t be billed again), you can feel free to reach out if you’d like a refund of your last month’s subscription.

I want everyone to feel like they got much more value from the newsletter than they paid, even if what they paid was such a small amount, so I’m more than happy to provide refunds to monthly subscribers. It’s absolutely no problem at all — just send me an email.

Thanks again for taking the time to read the newsletter. I have stats on how often these emails are read by folks, how much time is spent poking around the archives, etc. and it’s been fantastic to see how much the newsletter has been enjoyed. I also appreciate all the kind emails I’ve received — they always meant a lot to receive.

Best,

Zach